Some links may be affiliate links. We may earn a small commission at no extra cost to you.

Information may change over time and should be verified with official providers. We are not responsible for any decisions made based on this content.

Is Nationwide Pet Insurance Actually Worth It? What 500+ Pet Owners Really Think

Who Is This Blog For?

This blog is for you if you want to know if Nationwide Pet Insurance fits in your situation. Maybe you are here to compare it with other companies. Maybe you have heard mixed things about it, and you are confused. Maybe your pet is getting older, and you are wondering if insurance is still worth it. Or maybe you have had a bad experience with another company before, and you want to know if Nationwide is different or the same.

If any of these things match your condition, keep reading. This is written specifically for people in your position.

Who Should NOT Read This?

Don’t read this blog if you want to hear that pet insurance is always a good idea. This blog is not here to convince you to buy anything. This blog is to show real situations where insurance helps and real situations where it doesn’t. So if you just want to know good things instead of reality, you should not read this blog.

Also, skip this if you’ve already decided to get insurance and you don’t want anyone poking holes in that decision. That’s completely fair. Not everyone wants to read stuff that might make them second-guess themselves.

What You’re Actually Going to Learn Here

By the time you finish reading this blog, you’ll know the real pricing (not the “$25/month” marketing), what happened to 100,00 people whose insurance got cancelled, how much you’ll actually spend over 10 years, when insurance makes sense versus when it’s just losing money, how insurance companies deny claims, what to do if your claim gets rejected, and how Nationwide compares to other companies when you actually do the math.

You’ll also know whether insurance is good for your specific situation, not just whether it’s good in general. Your situation.

Introduction

Nationwide Pet Insurance is not new in the industry. They have been around since 1982, which is over 40 years. But when I analyzed their official plan documents and industry reports(like NAPHIA and AVMA), one thing became crystal clear: this policy does not fit for everyone. In this review, I have highlighted things that are beyond the marketing hype that can affect your premium and your pet’s health.

How I Researched This

I pulled plan details directly from Nationwide’s official website. I cross-checked coverage terms and pricing data using NerdWallet’s 2026 Nationwide review, CNBC Select’s review, U.S. News & World Report’s 2026 Nationwide overview, and Bankrate’s independent analysis. For industry benchmarks, I used NAPHIA’s 2025 State of the Industry Report, the most comprehensive data set on U.S. pet insurance, covering approximately 99% of written premiums in North America. For the cancellation and lawsuit facts, I used CBS News, Experian, and court filings reported by TopClassActions.com.

No affiliate links. No sponsored content. Everything below has a source you can check.

Nationwide’s Coverage – What You Actually Get

Nationwide offers a few different types of plans, but remember that not all of these have equal value. Some options can save your money, while some plans have hidden traps that can cost you extra money.

Whole Pet Plan:

This is Nationwide’s best and gold standard plan. It covers comprehensive options for accidents, illness, hereditary problems, and even covers behavioral treatments. You have to pay a $250 fixed annual deductible, and you can choose 50-70% reimbursement, whose annual limit is $10,000.

If you’re going with Nationwide for a dog or cat, this is realistically the only plan worth your money. It pays based on your actual vet bill, not a generic chart.

Major Medical Plan (The Hidden Trap):

This is Nationwide’s mid-tier plan. This plan is highly marketed, but this plan is the biggest trap in the pet insurance world. This plan clearly denies paying a flat percentage. Instead, the nationwide benefit schedule has made a fixed benefit schedule, where rates of every disease are already fixed.

For example, if your vet charges $5,000 for a complex surgery and you are calm. But the Nationwide chart says ” we’ll pay only $1,200 for this surgery”, now you are paying the remaining $3,800 out of pocket. If you want to keep yourself away from such shock, do not choose this plan.

Modular Plan:

This plan is new and customizable. This plan is best for people who want to control their premiums themselves. You can choose if you just want accident coverage, or if you want to add illness as well. You can decrease your premium by increasing deductibles from $250 to $1,000.

Wellness Add-On:

This plan covers vaccines, annual checkups, and teeth cleaning for your pet. This sounds good in hearing, but when you do mathematics, then you’ll know reality.

The extra money you pay for an add-on to the insurance company is equal to the money you spend going to the clinic at the end of the year. This is not a discount.

Exotic Pet Coverage (Nationwide’s True Superpower 🏆):

This part is where Nationwide leaves behind every other insurance company. If you have a parrot, rabbit, guinea pig, tortoise, or snake, then you may know how expensive and difficult to care for. Not a single famous brand touches this type of pet.

If you are a bird or reptile parent, then no other insurance company will cover you. Nationwide is your savior here. You don’t need to look for any other insurance company; this is your only solution.

Source: Nationwide Pet Insurance official plans page

Source: NerdWallet Nationwide Review

The 2024 Cancellation and the 2025 Lawsuit (The Full Story)

This is the part that most of the pet insurance reviews skip or soften. But I think you should know this before buying a plan from Nationwide.

In June 2024, an announcement shocked every pet owner in America. Nationwide cited increasing vet expenses and refused to renew 100,000 policies. This continued since the summer of 2025. They claimed that they didn’t remove it because of pets based on breed, because their new business model could not bear their expenses.

Just imagine how those pet parents felt who paid premiums to Nationwide every month for 8-10 years, and when their pet got old, and they needed it most, the company refused to pay.

Source: CBS News, June 2024

The story didn’t end here. In June 2025, a Class Action Lawsuit (Silberman et al. v. Nationwide) was filed in the Massachusetts federal court. The case is that when people bought Nationwide’s “Whole Pet” policy, then it was clearly written on the page of Nationwide’s FAQ page that it would “never drop because of age” if you had registered your pet before the age of 8 years.

The plaintiffs claimed that Nationwide first promised “Lifetime” coverage, and when the pets became seniors and needed expensive treatment, the company refused to pay to save itself from loss.

Source: TopClassActions.com, June 2025

The lawsuit is ongoing, and Nationwide has not been found liable. But what happened is a documented fact, not a rumor. If you are expecting 8 to 12 years of coverage for your pet, then you should know what this company does in times of need.

There is really financial pressure on insurance companies. According to NAPHIA reports, U.S insurance companies paid $3.07 billion in claims in 2024, which is 23.6% more than in 2023. Inflation is real, but it is a pity that Nationwide implemented this inflation on its 100,000 old and loyal customers.

Source: NAPHIA 2025 State of the Industry Report

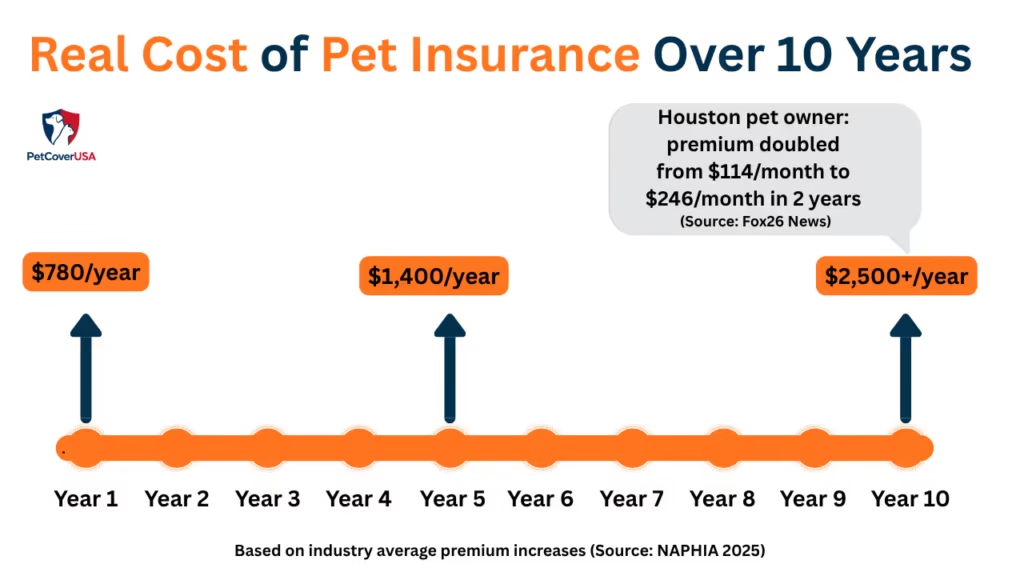

The Real Cost (What You’ll Actually Pay)

Nationwide’s marketing uses attractive words like “starting at,” which is far from reality. Here’s what verified data actually shows.

According to NAPHIA’s 2025 industry report, the average annual accident-and-illness premium in America for a dog is $749 (nearly $62 per month) and for cats is $386 (nearly $32 per month).

These are not just numbers. This is the basic expense that you have to pay under any condition. Even if your pet is healthy for the whole year.

Source: MoneyGeek analysis of NAPHIA 2025 SOI

According to NerdWallet’s pricing data, if you start insurance with Nationwide, the starting premium for dogs is nearly $50 per month, and for cats is $26 per month. But remember, this is just an “entry point”, because as your pet gets older, or your ZIP code changes, your premium will increase suddenly.

Source: NerdWallet Nationwide Pet Insurance Review

A real-world example of premium growth is that of a pet parent from Houston. While giving an interview to Fox 26 News, they said that the monthly premium for her Chow dog Bo, in 2022, was $114, which became $246 per month in just two years(2024).

The most shocking thing is that they didn’t file any claim in two years, and their pet has no pre-existing condition. Just imagine how an average person’s budget is affected when his monthly expenses are more than double without any reason.

Source: Fox 26 Houston, June 2024

The premium for pet insurance never remains fixed. According to the data from the Bureau of Labor Statistics (BLS), the Consumer Price Index of veterinary services is increasing from 7.6% to 7.9% every year, which is more than general inflation

When treatments become expensive in clinics, Insurance companies increase the premiums, and all the burden is on your pocket.

Source: MoneyGeek, citing Bureau of Labor Statistics data

According to a 2024 Forbes Advisor poll, 42% pet owners said that they’ll be in debt if they receive a $999 or below vet bill.

People buy insurance so they can save themselves from a $999 debt, but when companies like Nationwide increase their monthly premiums from $200 to $250, the real meaning of insurance fades. People think that they should save money instead of paying a premium.

Source: Referenced in classaction.org Nationwide lawsuit coverage

Nationwide vs. Competitors (Verified Side-by-Side)

This table is built completely from published plan details and independent reviewer data.

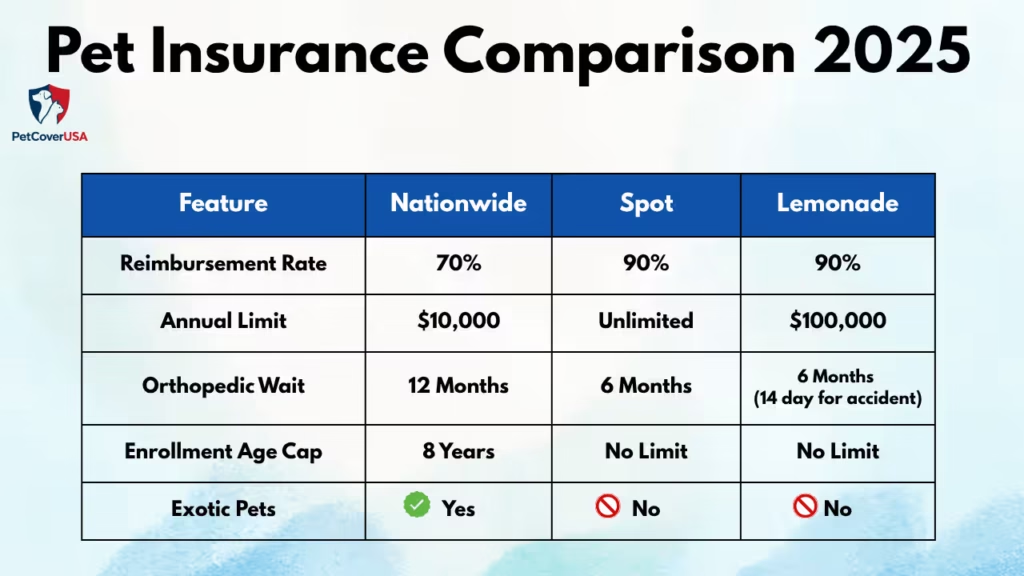

| Feature | Nationwide (Whole Pet) | Spot Pet Insurance | Lemonade Pet Insurance |

|---|---|---|---|

| Reimbursement rate | 50% or 70% (up to 80% on Modular plan) | Up to 90% | 60%, 70%, 80%, or 90% |

| Annual deductible options | $250, $500, $1,000 | $100–$1,000 | $100, $250, $500, $750 |

| Annual coverage limit | Up to $7,500 (Whole Pet); up to $10,000 (Modular) | Up to unlimited | Up to $100,000 |

| Orthopedic/cruciate waiting period | 12 months (most states) | 6 months (14 days with vet orthopedic exam) | 6 months (cruciate); 30 days (other orthopedic) |

| Exotic pet coverage | Yes (birds, reptiles, ferrets, rabbits) | No | No |

| Max enrollment age (dogs/cats) | 8 years for illness coverage; Whole Pet requires dogs ≥1 year | No upper limit | No upper limit |

| Cancer coverage | Yes (illness coverage available only for pets ≤8 years at enrollment) | Yes | 50% or 70% (up to 80% on the Modular plan) |

If you just read an affiliated review, then you’ll think that Nationwide is the best. But when we compare it with big companies like Spot and Lemonade pet insurance, then you’ll face such realities that can break your heart.

Nationwide’s most famous Whole Pet Plan may give you maximum reimbursement from 70% to 80%. In comparison, Spot and Lemonade offer reimbursement of 90%.

Just imagine, your pet gets an operation and the vet bill is $10,000. If you have Spot or Lemonade pet insurance, you’ll pay just $1,000 out of your pocket. But if you have Nationwide, then you have to pay $3,000 out of pocket. NerdWallet has also targeted this clearly, stating that Nationwide’s payout rates are lower than those of other brands. This 20% difference may shock you during a difficult time.

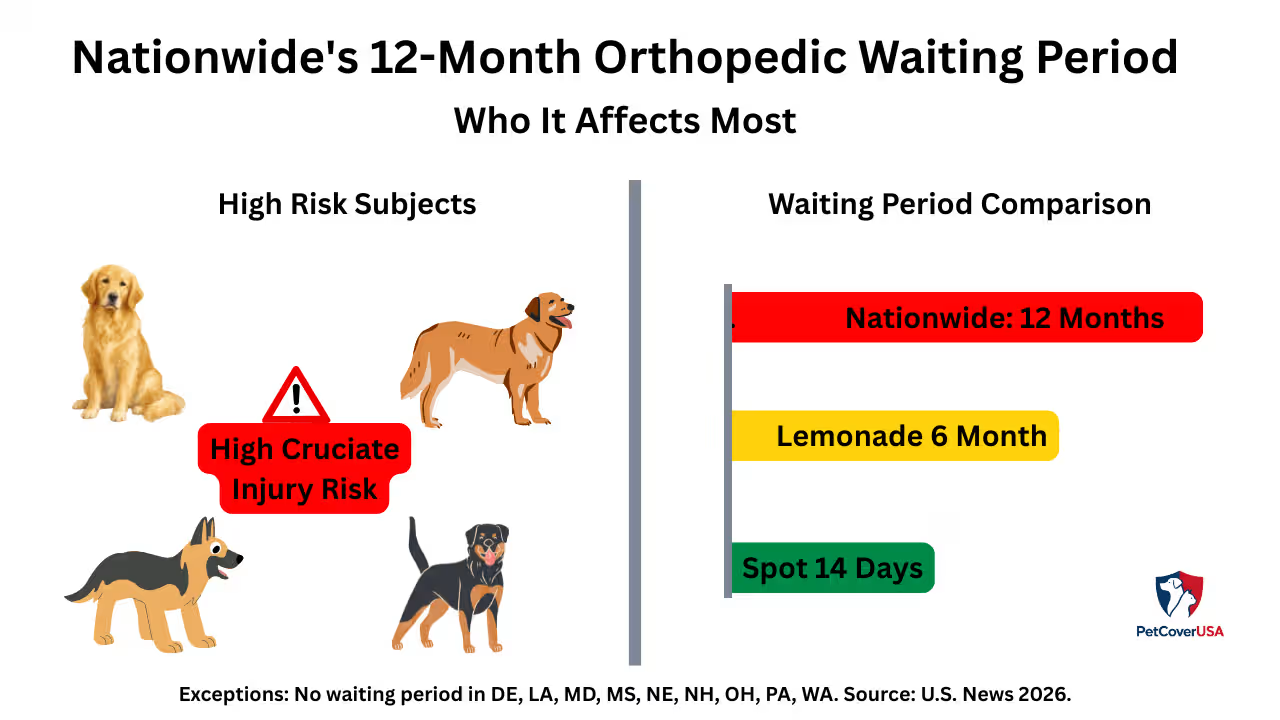

The orthopedic waiting period is the biggest hidden fault of Nationwide. Nationwide requires a 12-month waiting period for cruciate ligament and meniscal injuries in most states. This is the longest waiting period in the industry. In comparison, the waiting period for the cruciate ligament in Lemonade and Spot is 6 months (the standard accident waiting period is only 14 days).

If your pet is a Labrador, Golden Retriever, German Shepherd, or any breed like this, then you may know these breeds are more prone to bone or knee diseases. Now think, you bought insurance by thinking that your puppy will not get any problems, but Nationwide says they require a 12-month waiting period. Within this waiting period, if your dog tears a knee or ligament, then you’ll pay out of your pocket.

Sources: NerdWallet, CNBC Select, U.S. News, Spot Pet Insurance, MoneyGeek

The Enrollment Age Cap (Why It Matters More Than You Think)

Nationwide clearly refuses to register dogs and cats that are 8 or above on their standard plans. Even though it is not new to set such boundaries in the insurance industry, you need to understand its timing as a pet parent.

Dr. Patty Khuly (VMD, Vetstreet) writes about the importance of early enrollment.

“I’m a pet health insurance devotee, and if a veterinarian thinks it’s worthwhile to insure her animals, you should probably consider purchasing policies for your pets, too.”

Dr. Patty Khuly, VMD, Vetstreet

Dr. Patty highlights a very important topic, which is not less than a nightmare for pet parents, when their pet becomes senior, which is “Pre-existing Conditions”. Some companies have a policy that they only cover pre-existing conditions if it doesn’t appear for a specific period of time. something that becomes increasingly relevant for older pets.

Source: Dr. Patty Khuly, VMD, Vetstreet

AVMA (American Veterinary Medical Association) research says something interesting. Pet parents who have pet insurance, they act more on their vet’s recommended care, because the financial barrier is lower.

The matter of regret is that you lose your peace of mind and support when your pet need is most. When your pet becomes 8 years old, and you go to Nationwide for enrollment, it refuses to enroll.

If your pet is 8 years old and has no insurance, you don’t need to worry. You should focus on alternatives like Embrace or Spot instead of trying to get into Nationwide. The good thing is that these companies have no age limit for enrollment. They will gladly welcome and protect your senior pet.

Source: AVMA

Who Should Buy Nationwide And Who Shouldn’t

Buy Nationwide if:

- If you have an exotic pet like birds, reptiles, rabbits, ferrets, or guinea pigs. Nationwide is the clearest and unique advantage in the market.

- Your pet is young (under 3 years old), and you want an insurer with a 40+ year track record in the U.S.

- Your employer offers Nationwide as a group benefit (My Pet Protection), which often carries much better pricing and 90% reimbursement options.

- You want to insure multiple pets. Nationwide offers a 5% multi-pet discount for 2-3 pets, which bumbps unpto 10% if you insure 4 or more.

Don’t Buy Nationwide if:

- Your pet is over 7 years old and currently uninsured. They won’t accept new enrollments.

- Your dog is a Lab, Golden Retriever, German Shepherd, or another orthopedic-prone breed. The 12-month cruciate waiting period is a genuine coverage gap.

- You want high reimbursement rates. Spot and Lemonade both offer up to 90% vs. Nationwide’s 70% ceiling on Whole Pet.

- You want unlimited annual coverage. Nationwide caps at $10,000/year.

- The 2024 cancellations concern you; that concern is legitimate and worth factoring in.

Frequently Asked Questions About Nationwide Pet Insurance

Does Nationwide pet insurance cover pre-existing conditions?

No. Like every major U.S. pet insurer, Nationwide does not cover pre-existing conditions. Clinical signs before policy start or during waiting period can be used for exclusion.

What is Nationwide’s waiting period for knee injuries?

In most states, Nationwide requires a 12-month waiting period for cruciate ligament and meniscal injuries. Some states have exceptions.

Can Nationwide cancel my pet insurance?

Yes. Around 100,000 policies were canceled between 2024–2025 due to rising veterinary costs. Legal challenges are ongoing.

Is Nationwide good for senior dogs?

No for new enrollments. They generally stop accepting pets over 8 years old on standard plans.

What is the difference between Whole Pet and Modular plan?

Whole Pet has fixed coverage terms while Modular allows customizable deductible, reimbursement, and coverage options.

Is the pet insurance industry growing?

Yes. The industry reached $4.74B in 2024 with 21% growth, but only 3.9% of pets are insured, leaving room for expansion.

Final Verdict

After reviewing all things, I came to the point that:

Nationwide is not a bad company. They have been in the insurance industry for more than 40 years. Their Whole Pet plan is best for young pets, and for exotic pets, there is no comparison to Nationwide in the whole USA.

But if I think as a new customer, these three things will force me to think before buying Nationwide Pet Insurance:

The 70% limit on Whole Plan is low for facilities that Spot and Lemonade are offering at the same price. Just imagine if your pet gets $6,000 surgery, so because of 20% difference, you have to pay $1,200 out of your pocket.

If you have a breed that is prone to knee or ligament disease, then you are helpless for 12 months with Nationwide. The company has a lock on the most expensive treatment

I can’t claim that Nationwide will cancel your policy as well. But they have proved that when a company faces financial pressure, it can leave its customers for its own profit. You should know this reality as a pet parent.

My Final Recommendation

If you have an exotic pet. Then you should definitely choose Nationwide, because there is no better way in the U.S. market.

If your puppy is less than 4 years old, then you should check Spot or Lemonade first, where you’ll get better reimbursement and a shorter waiting period for ligament treatment will less than with Nationwide.

If you are already on Nationwide and everything is fine, then I’ll recommend that you stay there. If you change company, all the conditions your pet has appeared during that time period will be pre-existing for the new insurance company and will not be covered.

The biggest mistake in pet insurance is not to choose wrong company; instead, it is the delay in making a decision. If once a disease is written in your pet’s medical record, not a single company in the U.S will cover it. The best policy is always one that we buy before anything happens.

Primary Sources Used in This Article:

- Nationwide Pet Insurance official plans

- NerdWallet Nationwide Pet Insurance Review (2026 update)

- CNBC Select Nationwide Review

- U.S. News Nationwide Insurance Overview (2026)

- Bankrate Nationwide Pet Insurance Review

- NAPHIA 2025 State of the Industry Report

- AVMA reporting on NAPHIA 2025 data

- AVMA on pet insurance and veterinary care

- CBS News Nationwide drops 100,000 pet policies

- Fox 26 Houston Real policyholder premium increase

- TopClassActions.com 2025 Nationwide class action lawsuit

- ClassAction.org Nationwide Whole Pet lawsuit details

- Experian What happens if pet insurance is canceled

- MoneyGeek NAPHIA 2025 market penetration analysis

- MoneyGeek ACL cruciate waiting periods by insurer

- Spot Pet Insurance Waiting period comparison

- Dr. Patty Khuly VMD Vetstreet Pet Insurance Checklist

📅 Last Updated:

Research & Editorial Process: This article was independently researched and written using publicly available insurer policy documents, veterinary resources, and trusted third-party reviews. Information was fact-checked against primary sources where available.

📖 This article on Nationwide Pet Insurance is regularly updated to provide accurate, research-backed coverage information for pet owners.

About the Author

M. Nouman is an independent researcher and writer focused on U.S. pet insurance. He reviews insurer policy documents, coverage terms, waiting periods, reimbursement options, exclusions, and publicly available veterinary and regulatory resources to create clear, research-based guides. His goal is to simplify complex insurance information so pet owners can make informed decisions based on reliable sources rather than marketing claims. Articles are reviewed and updated as policies and industry information change.

Areas of Research: Pet Insurance Policies, Coverage Analysis, Policy Comparisons, Waiting Periods, Reimbursement Models, Policy Exclusions, Claims Education

Research insights and updates on Quora, LinkedIn, and Reddit.