Some links may be affiliate links. We may earn a small commission at no extra cost to you.

Information may change over time and should be verified with official providers. We are not responsible for any decisions made based on this content.

Top 5 Affordable Pet Insurance Plans in 2026: What Many Guides Don’t Highlight

The most affordable pet insurance plan is not always the one with the lowest monthly premium. After my research, I found that cheaper plans often cost you more at claim time through reimbursement caps, per-incident deductibles for chronic conditions, and rising premiums as your pet ages.

The Real Cost Picture: Why Vet Bills Are Now a Financial Emergency

Let me give you numbers that shocked me during my research: Some industry studies indicate that since 2021, prices for veterinary services have surged significantly, with estimates between 20% and 30%, exceeding average inflation rates in many areas. That is not a small difference; it shows that the real cost of owning a pet has changed.

Here are the real numbers I found:

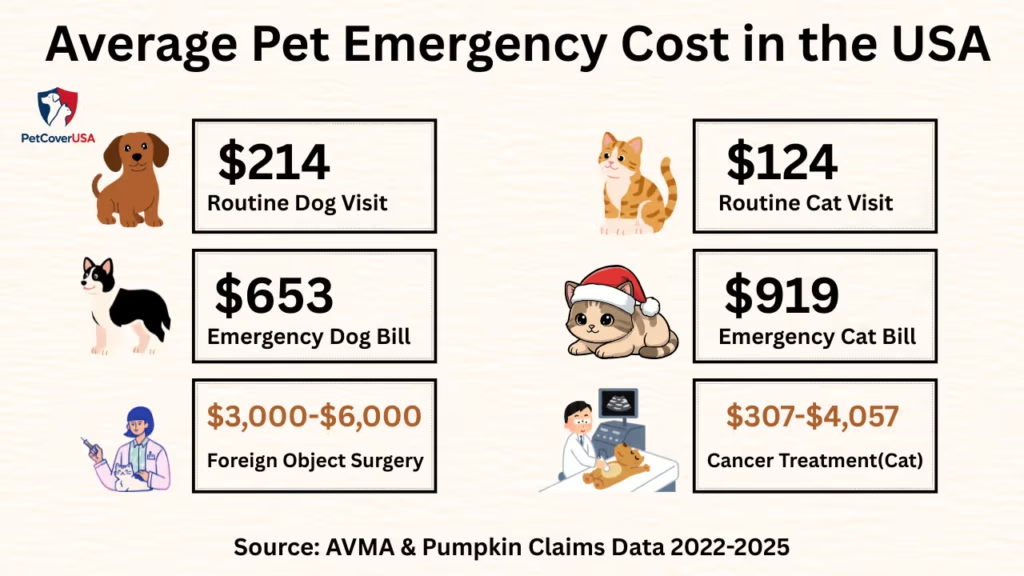

- Average routine dog vet visit: $214 (AVMA, 2024) Source: Pawlicy Advisor / AVMA (2024)

- Average emergency vet bill for dogs: $653 (Pumpkin claims data) Source: Pumpkin Insurance Claims Data (2022–2025)

- Average emergency vet bill for cats: $919 (Pumpkin claims data)

- Average annual vet cost inflation 2021–2024: 7.43% Source: Companion Pet Magazine

And those are averages. A dog that swallows a foreign object and needs surgery? You are looking at $3,000-$6000 easily. Similarly, do you need Cancer treatment for a cat? Claims data from Pumpkin shows the cost between $307 and $4,057 for just emergency components, even before treatment starts.

Here’s something a real vet told me that I think every pet owner needs to hear:

“I absolutely think pet insurance is worth it, and I have insurance on all of my animals. I never want someone to have to decide between their pet’s life or having money to live.”

Dr. Adams, DVM

Source: Rover.com

Here’s a stat that really shows the reality: only 5.46% of dogs and 2.04% of cats in the U.S. have insurance. Most pet owners are just one emergency away from a very difficult decision. Source: NAPHIA 2025 State of the Industry Report

A study found that 50% of pet owners without insurance worry about how they would pay a vet bill if their pet gets sick. That means half of them are constantly stressed about unexpected costs. Source: Companion Pet Magazine

Cheapest Affordable Pet Insurance Plans: Real Premiums, Real Coverage

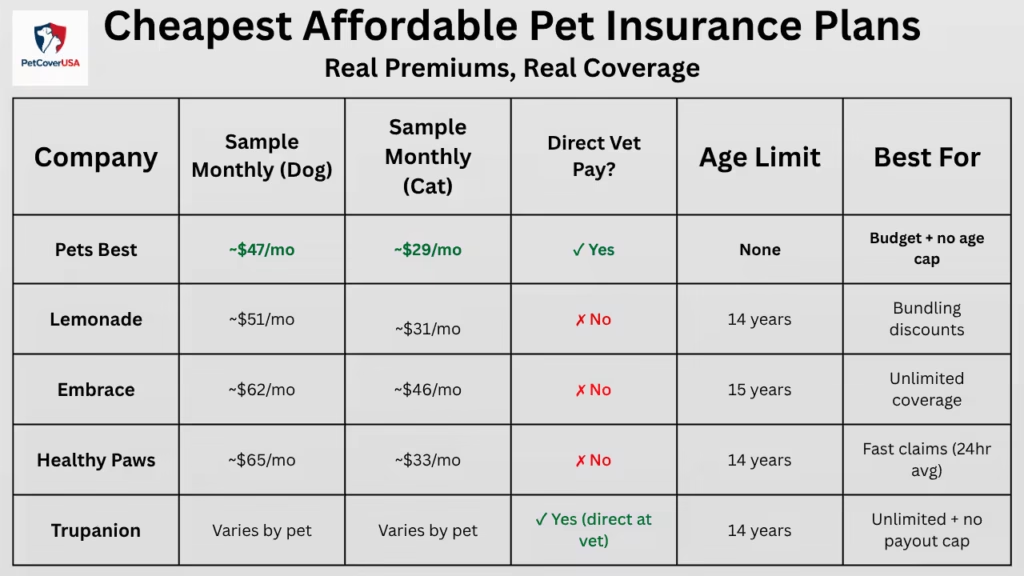

Here’s what I found after looking past the marketing hype. These are sample monthly rates for a typical case: a 2-year-old mixed-breed dog, $250 deductible, 90% reimbursement, accident-and-illness coverage. Your actual cost will depend on your dog’s age, breed, and where you live.

| Company | Monthly (Dog) | Monthly (Cat) | Direct Vet Pay | Age Limit | Best For |

|---|---|---|---|---|---|

| Pets Best | ~$47/mo | ~$29/mo | ✓ Select vets | None | Budget + no age cap |

| Lemonade | ~$51/mo | ~$31/mo | ✗ No | 14 years | Bundling discounts |

| Embrace | ~$62/mo | ~$46/mo | ✗ No | 15 years | Unlimited coverage |

| Healthy Paws | ~$65/mo | ~$33/mo | ✗ No | 14 years | Fast claims (24hr avg) |

| Trupanion | Varies | Varies | ✓ At checkout | 14 years | Unlimited + no payout cap |

Source: U.S. News & World Report Pet Insurance Rate Study (2025) — rates are averages across 51 U.S. jurisdictions.

But here’s what I want you to notice: the cheapest monthly premium is not automatically the most affordable plan. I’ll show you exactly why in the next section.

The Deductible Trap: Annual vs. Per-Incident (Most Buyers Get This Wrong)

This is one of the most overlooked details in many comparison articles I’ve read, and it can cost you thousands. Most blogs list deductible amounts ($100, $250, $500) but never explain the type of deductible. There are two fundamentally different structures, and which one you have changes everything.

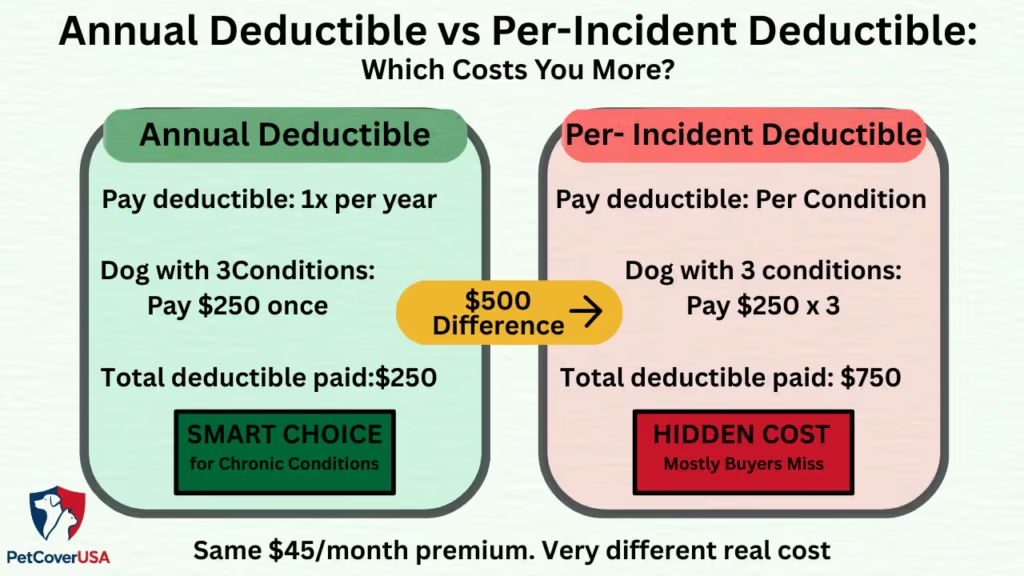

Annual Deductible

You only pay your deductible once per year, no matter how many issues your pet has. So if your dog gets allergies, an ear infection, and a sprained leg in the same year, you still pay the deductible just once. After that, all covered claims are reimbursed at your chosen rate.

Per-Incident Deductible

You pay the deductible for every separate condition or incident. That same dog with allergies, an ear infection, and a sprained leg? You pay the deductible three separate times. If your pet has a chronic condition like diabetes or allergies that requires repeated treatment, this structure makes your plan dramatically more expensive in practice than the premium suggests.

Here’s the real math:

If a dog has chronic allergies and your plan charges a $250 deductible per incident, you could end up paying $750 or more in a year for three visits before insurance covers anything. A “cheap” $45/month plan can become very costly when claims happen. Always ask which deductible type you’re being offered before you sign anything.

Trupanion, for example, uses a per-condition lifetime deductible; you pay it once for a condition and never again. For pets with ongoing health issues, this can be much cheaper long-term, even if the monthly premium is higher.

The Pre-Existing Condition Reality: What Reddit Taught Me That Review Sites Won’t Tell You

I have spent specific time going through real pet insurance claims experiences shared by real users, and the pre-existing condition issue comes up more than anything else. Here is what is actually happening:

A real user story from r/petinsurancereviews:

A Reddit user’s cat was drinking a little more water than usual, so the vet wrote a note about it. They tested the cat for hyperthyroidism at the time, and it came back negative. A year later, the cat was actually diagnosed with hyperthyroidism.

When the owner filed a claim, MetLife denied it because the cat showed that symptom during the 14-day waiting period, which counts as a pre-existing condition, even though there was no diagnosis at the time and the test was negative.

Basically, the insurer treated any prior symptom as a red flag for a pre-existing condition, regardless of whether the cat was actually sick back then.

Source: r/petinsurancereviews “DO NOT use Metlife” (verified user post, 2025)

This is the trap most buyers never see coming: many insurers go by symptoms, not diagnoses. A note in your pet’s file saying “seemed lethargic” can be used to deny future claims for conditions that weren’t even diagnosed yet.

How to Protect Yourself

- Enroll your pet before their first vet visit when possible. Zero medical history means zero pre-existing ammunition

- Ask your insurer specifically: “Do you go by symptoms or confirmed diagnosis when evaluating pre-existing conditions?”

- Request a written pre-existing condition review before your waiting period ends; some companies offer this upfront

- If your pet had a curable condition like Giardia, ask specifically whether it can be covered after a documented symptom-free period

- Read your policy’s exact definition of “pre-existing”, it varies significantly between companies

Here’s what a real veterinarian said about the value of insurance that actually pays at claim time:

“We have so many clients that have Trupanion… Every time a patient is able to receive complete and expeditious care, we reduce suffering, owner stress, and worry.”

Dr. Pamela Kaiser, DVM, Jacksonville, FL

Source: Trupanion.com (Veterinarian Testimonials)

The Premium Creep Problem: Your “Affordable” Plan May Double by Year 4

This is the thing that most of the comparison blogs do not tell you. And based on real user experiences that I have collected, it is one of the most common reasons people end up paying out of pocket, right when their pet needs coverage the most.

Real user research from r/petinsurancereviews:

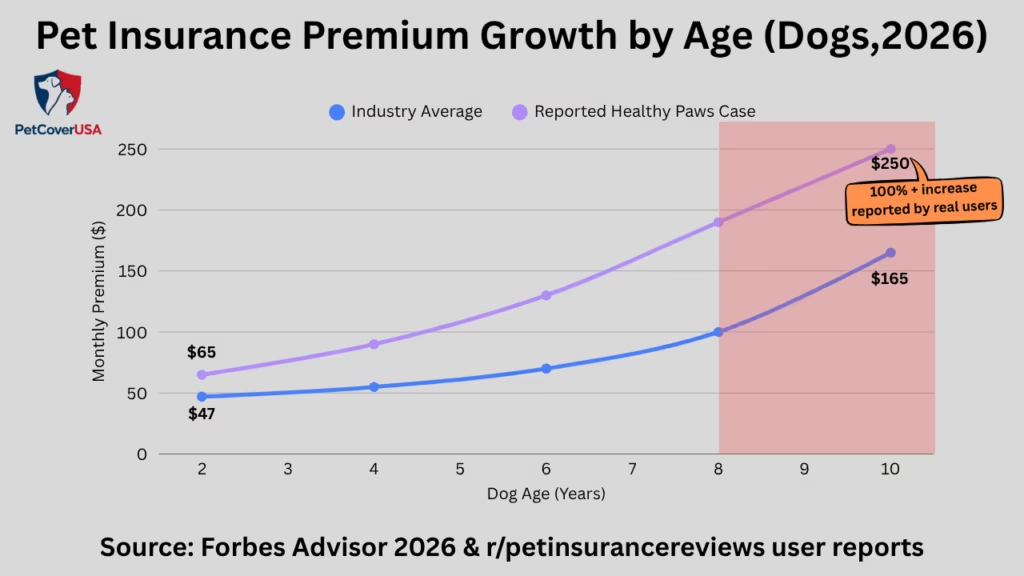

However, while users of Healthy Paws report increases of up to 100% or more in premiums over the years, these are individual cases and not data that have been officially disseminated by the company. One user saw their 9-year-old lab’s premium jump from $118/month to nearly $250/month, for a dog who has only a minor claims history( ear infections, nausea). The user’s comment: “Now, these things will all be pre-existing, so we can’t really go somewhere else.” That last line is the real problem. They couldn’t leave even if they wanted to.

Source: r/petinsurancereviews “Don’t get Healthy Paws! INSANE policy price increases!” (verified post, 2025)

The numbers show this isn’t just one company being tricky. Several industry sources show a remarkable increase in dog accident and health insurance premiums from 2019 to 2024, with some results reflecting a rise of 25% to 30% in average levels, and that’s before any extra age-based increases some insurers tack on.

Source: CNBC Select (Is Pet Insurance Worth It in 2026?)

What to Look For to Avoid Premium Shock

- You should ask directly: “What is your average annual premium increase for a dog aged 2 to 8?”

- Check whether increases are age-based (your pet’s birthday) or claims-based; both happen at different companies

- Trupanion’s stated policy is that they don’t raise rates specifically based on your pet’s age, though rates can still change based on broader actuarial data in your area

- Look at the insurer’s underwriter stability; companies that switch underwriters often see the most dramatic rate changes

- Lock in young: a policy for a 2-year-old dog costs an average of ~$51/month (unlimited coverage); the same plan for a 7-year-old averages ~$95/month

Source: Forbes Advisor (Cheapest Pet Insurance Companies 2026)

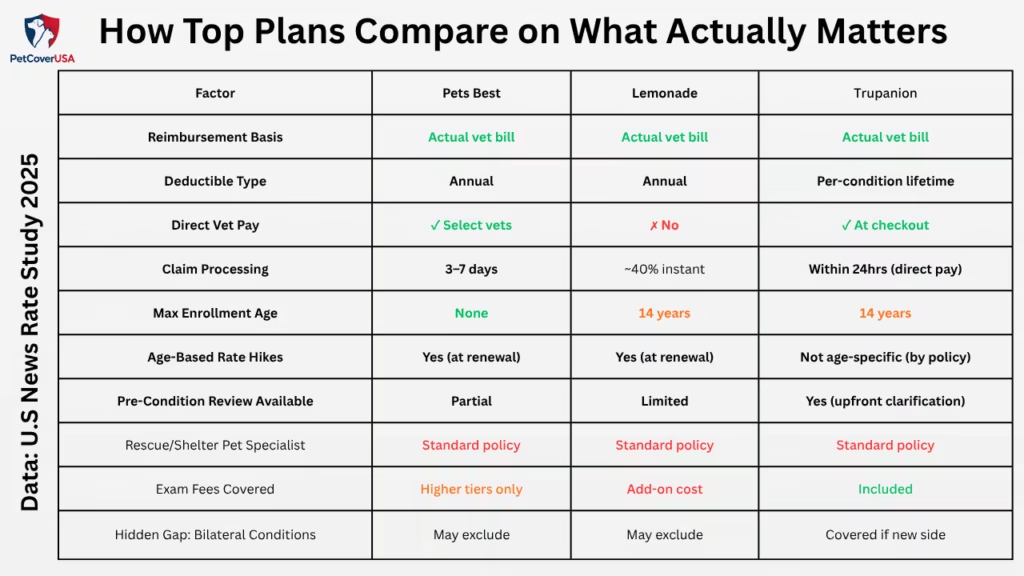

Deep Research Table: What Top Plans Actually Look Like Where It Matters

Every competitor blog shows you price and deductible options. Here’s what my research found: Many comparison articles do not address issues that are key in deciding whether a claim will be honored.

| Factor | Pets Best | Lemonade | Trupanion |

|---|---|---|---|

| Reimbursement Basis | Actual vet bill | Actual vet bill | Actual vet bill |

| Deductible Type | Annual | Annual | Per-condition lifetime |

| Direct Vet Pay | ✓ Select vets | ✗ No | ✓ At checkout |

| Claim Processing | 3–7 days | ~40% instant | Within 24hrs (direct pay) |

| Max Enrollment Age | None | 14 years | 14 years |

| Age-Based Rate Hikes | Yes (at renewal) | Yes (at renewal) | Not age-specific |

| Exam Fees Covered | Higher tiers only | Add-on cost extra | Included |

| Pre-Condition Review | Partial | Limited | Yes (upfront) |

One thing that stands out across all three companies: Most of the major pet insurance companies do not provide special onboarding for rescuing pets. If your dog came from a shelter, with vet records you didn’t create and conditions you weren’t aware of, you’re stuck with the same standard policy as someone who raised their pet from a puppy. And that leads to the next point.

If You Have a Rescue Pet: The Shelter Records Problem Nobody Talks About

This keeps coming up in real user research, and you won’t see it mentioned in competitor articles. Here’s the scenario: you adopt a rescue dog or cat. The shelter’s vet treated the animal beforehand, maybe for Giardia, a respiratory infection, or an injury. You didn’t pick those vets, and you might not have even known about the visits until you got the adoption paperwork. Now those records exist, and insurers can and do use them to deny future claims.

Real user story from r/petinsurancereviews:

A user described adopting a puppy that had tested positive for Giardia at the rescue(treated and resolved before adoption). They were really worried that any future gastrointestinal issue, even a totally unrelated one, might be linked back to that original shelter record and get denied.

Source: r/petinsurancereviews “One more question before choosing a plan – puppy giardia in rescue” (verified post, 2025)

Practical Steps for Rescue Pet Owners

- Enroll your rescue pet in insurance before their first post-adoption vet visit with your own vet; this creates a cleaner baseline.

- Ask the shelter for a full copy of all vet records before enrolling; you need to know what’s documented before an insurer sees it.

- Fetch Pet Insurance is recognized by multiple Humane Society organizations for shelter and rescue pets and covers some common pre-existing conditions from day one for pets adopted from participating shelters.

- If a condition was fully treated and resolved (like Giardia), ask your insurer to document in writing that it will be treated as cured; most insurers require a symptom-free period of 6–12 months.

Source: Fetch Pet Insurance (Rescue & Shelter Pet Coverage)

How to Actually Save Money on Pet Insurance (Beyond Just Comparing Premiums)

Most guides stop at “compare quotes.” Here’s what actually moves the needle in my research:

Step 1: Insure Young, Insure Early

The data is clear. A plan for a 2-year-old dog costs about $51 per month for unlimited coverage, while the same plan for a 7-year-old dog costs around $95 per month. That’s about $528 more per year.

Getting coverage early also helps you avoid future conditions being labeled as pre-existing.

Step 2: Choose Annual Pay Over Monthly

Lemonade offers a 5% discount if you pay yearly and removes the monthly billing fee. It may seem small, but it adds up over time.

Step 3: Stack Multi-Pet Discounts

Almost every big pet insurance company offers a 5-10% multi-pet discount, so it may be helpful if you have multiple pets. Lemonade offers up to 10% on both policies. Pets Best offers 5%. These discounts are not mentioned in advertisements, so you have to ask your pet insurance company directly.

Step 4: Match Your Deductible to Your Pet’s Actual Risk

If you have a young, healthy mixed-breed dog, a higher deductible, like $500, makes sense because you’re mainly covering big emergencies and saving on monthly costs.

But if you have a breed like a French Bulldog that is more likely to have health issues, a lower deductible is better because you’ll reach it more often.

Step 5: Check Your Employer Benefits

Pet insurance is now often offered as a workplace benefit. Check with your HR team, as you might get discounted group rates. This is becoming more common in larger companies.

Step 6: Submit Claims Correctly the First Time

Based on advice from a real claims adjuster: always submit a full itemized invoice, not just a summary. Include all medical records from the past 12 months for your first claim, and make sure pharmacy orders show “shipped” status with your pet’s name. Missing details can delay payments and may lead to extra reviews that bring up pre-existing condition issues.

Source: r/petinsurancereviews “tips from an adjuster” (verified post, 2025)

Frequently Asked Questions (FAQ’s)

What’s the most affordable pet insurance plan overall? +

Based on sample rate data across 51 U.S. jurisdictions, Pets Best has the lowest average monthly premium for both dogs (~$47/mo) and cats (~$29/mo) for a standard accident-and-illness plan. However, for pets with chronic conditions, Trupanion’s per-condition lifetime deductible often works out cheaper in the long run despite higher monthly premiums. The right answer genuinely depends on your specific pet.

Can pet insurance deny a claim for something my vet only mentioned once? +

Yes — and this is more common than most people realize. Some insurers base pre-existing condition decisions on documented symptoms, not confirmed diagnoses. A single vet note mentioning a symptom (even during your waiting period, even if never formally diagnosed) has been used to deny claims. Always ask your insurer explicitly whether they use a symptom-based or diagnosis-based standard.

Is pet insurance worth getting for a rescue pet with unknown history? +

Yes — but timing and company choice matter enormously. Fetch Pet Insurance specifically covers some pre-existing conditions from day one for newly adopted pets from participating shelters. For other insurers, enroll before your first post-adoption vet visit to establish the cleanest possible baseline.

How much does pet insurance cost for a senior dog? +

Significantly more. Unlimited coverage with a $250 deductible and 80% reimbursement for a 2-year-old dog averages ~$51/month. For a 7-year-old dog, that climbs to ~$95/month. By age 9–10, some insurers have raised premiums to $200–$250+/month based on real user reports. The best way to avoid senior pet premium shock is to insure young and never let the policy lapse.

What does “usual and customary” reimbursement mean? +

Some insurers reimburse based on what they determine is the “usual and customary” cost for a procedure in your area — not what your vet actually charged. If your vet’s rates are above average (urban areas, specialist care), you’ll receive less than your expected reimbursement percentage. Most major U.S. pet insurers (Pets Best, Lemonade, Trupanion) reimburse based on your actual vet bill — always confirm this before you buy.

Are all the big pet insurance brands actually independent companies? +

No — and this surprises a lot of buyers. IPH (Independence Pet Holdings) is the parent company of multiple well-known brands including ASPCA Pet Health Insurance, Pets Best, Embrace, Spot, Pumpkin, and Figo among others. They may have different policies and pricing but share ownership. This is worth knowing when you think you’re comparing completely independent insurers.

Final Verdict: What “Affordable” Actually Means

After analysing all the data, real user stories, insurance companies’ fine print, and industry reports, here is my honest conclusion:

The affordable pet insurance plan is the one you can still afford to keep when your pet is 9 years old, that really pays when you file a claim, and that does not surprise you with pre-existing conditions denials for symptoms your vet mentioned years ago.

- If you have a healthy pet under the age of 3, then Pets Best gives you the lowest entry cost with no enrollment age cap

- If you have a rescue pet, then Fetch is specially designed for shelter-pet coverage that addresses the records problem

- If your pet has a long-term chronic condition, then Trupanion’s per-condition deductible structure often wins on total annual cost

Choosing a plan now: Get at least three quotes and ask:

- The type of deductible

- The reimbursement basis

- The average annual renewal increase rate

Asking these three questions alone gives you an advantage over 90% of buyers.

Related Pet Insurance Guides

Explore our in-depth pet insurance resources to better understand coverage options, costs, and plan differences across the USA.

-

Lemonade Pet Insurance Review 2026

A detailed breakdown of Lemonade’s coverage, pricing structure, claim speed, and limitations. Useful for pet owners comparing modern, app-based insurance providers.

-

Affordable Pet Insurance Plans for Dogs and Cats

An overview of budget-friendly pet insurance options available in the U.S. Covers cost ranges, plan types, and who these plans are best suited for.

-

Best Pet Insurance for Older Dogs

Compares insurance providers that offer coverage for senior dogs. Focuses on age limits, premium increases, and chronic condition support.

-

Pet Insurance With the Most Complete Coverage

Explains what “full coverage” really means in pet insurance. Highlights policy exclusions, coverage limits, and realistic expectations.

-

Pet Insurance With No Waiting Period in the USA

Reviews plans that offer immediate or reduced waiting periods. Ideal for pet owners needing faster access to coverage.

-

Pet Insurance and Pre-Existing Conditions Explained

A clear explanation of how insurers define and handle pre-existing conditions. Helps pet owners avoid claim denials and policy misunderstandings.

-

Nationwide Pet Insurance Plans and Costs

A comprehensive guide to Nationwide’s pet insurance policies. Covers pricing, coverage details, and plan suitability.

-

Pet Insurance That Covers Dental Care for Dogs

Explains which insurers include dental illness and injury coverage. Important for breeds prone to dental health issues.

Still Confused? Leave a question below!

📅 Last Updated:

About the Author

M. Nouman is an independent researcher and writer focused on U.S. pet insurance. He reviews insurer policy documents, coverage terms, waiting periods, reimbursement options, exclusions, and publicly available veterinary and regulatory resources to create clear, research-based guides. His goal is to simplify complex insurance information so pet owners can make informed decisions based on reliable sources rather than marketing claims. Articles are reviewed and updated as policies and industry information change.

Areas of Research: Pet Insurance Policies, Coverage Analysis, Policy Comparisons, Waiting Periods, Reimbursement Models, Policy Exclusions, Claims Education

Research insights and updates on Quora, LinkedIn, and Reddit.