Some links may be affiliate links. We may earn a small commission at no extra cost to you.

Information may change over time and should be verified with official providers. We are not responsible for any decisions made based on this content.

Embrace Pet Insurance Review 2026: The Truth Nobody Else Tells You

Embrace Pet Insurance is genuinely one of the pet insurance options out there that can be customized, and its wellness coverage is one step above most of its competitors. But there are some things that I want to tell you that, after reviewing hundreds of real customer experiences, that: your satisfaction with Embrace will largely depend on your pet’s medical history and whether you understand three very specific policy mechanics, the pre-existing condition definition, the bilateral exclusion rule, and what happens when you upgrade your coverage. You should understand those three things before you buy, and you will avoid most of the surprises people face at the time of a claim.

What Is Embrace Pet Insurance?

Embrace was founded in 2003 by Laura Bennett and Alex Krooglik, and it sold its very first policy to a cat named Lily in Chagrin Falls, Ohio, on October 10, 2006. For a very long time, Embrace Pet Insurance was an independent company known for its really flexible structure of policy in the market, where most of the insurance companies had a take-it-or-leave-it policy.

Here are things almost no review mentions, and I think it matter is that in late 2023, Embrace was acquired by JAB Holding Company for 1.5 billion. JAB is a German private equity group that now owns 21 pet insurance brands globally, which include FIGO, Pumpkin, and the Independence Pet Group. One ConsumerAffairs user, who flagged this, put it bluntly:” Users are concerned that mergers in the pet insurance industry could cause renewal premiums to increase, while others note that the extent of the increase depends on the policy and the specific location.” Source: CoverageR

I am not saying that this makes Embrace a bad product. But I think that you deserve to know from whom you are actually buying policy and why premiums have been increasing since 2023. Embrace’s policies are underwritten by American Modern, a Munich Re company, which adds a layer of financial stability. Yes, if you buy pet insurance from GEICO or USAA, it may actually be an Embrace policy behind the scenes. Source: Review.com

Today, Embrace has insured over 500,000 pets and processed more than 4.6 million claims. It operates in all 50 states and Washington, D.C as well. On paper, that is impressive. In reality, as you’ll see below, the experience is more mixed than it looks from the polished numbers.

Ratings & Research Methodology

In my research, I analyzed data from Trustpilot (10,599 reviews), ConsumerAffairs (4,820,000+ verified reviews), Better Business Bureau complaint filings from 2024–2026, and Reddit community discussions. I also reviewed Embrace’s official Terms & Conditions and FAQs directly. Here is how Embrace scores:

| Category | Score | Notes/Source |

|---|---|---|

| Overall Score | 4.1 / 5.0 | Trustpilot (10,601 reviews), WSJ 3.5/5, Yahoo 4/5 moneygeek+2 |

| Coverage Depth | 4.4 / 5.0 | Comprehensive accident/illness, alternative therapies; Consumers Advocate 4.4/5 petinsurer+1 |

| Cost & Value | 4.0 / 5.0 | Competitive premiums (~$46 cats, $73 dogs), but higher than some moneygeek+1 |

| Claims Experience | 3.2 / 5.0 ⚠️ | Mixed; Reddit/BBB complaints on denials (131 in 3 years) moneygeek+1 |

| Wellness Coverage | 4.6 / 5.0 | Up to $650 optional add-on, highly rated petinsurer+1 |

| Transparency | 3.8 / 5.0 | A+ BBB rating, clear terms, but claim issues moneygeek+1 |

The claims experience score deserves an explanation. Community talks on Reddit speak of both good and bad experiences of travelers using Embrace; however, these opinions are casual and are not formal statistics. That is a pattern I kept seeing across every platform I reviewed. The product itself is solid; the claims adjudication process is where things get complicated.

✅ Pros & Cons at a Glance

Pros

- Highly customizable deductible ($100–$1,000), reimbursement (70–90%), and annual limit ($5K–unlimited)

- Covers curable preexisting conditions after 12 months symptom-free

- Best-in-class Wellness Rewards covers GPS trackers, training, dental chews, and cremation

- Breed-specific and genetic conditions covered from day one (if no prior symptoms)

- No vet network restrictions, any licensed vet in all 50 states

- The orthopedic waiting period is reducible to 14 days via an optional exam

- 24/7 vet tech access via chat, video, or phone

- Apollo AI claims technology speeds processing by 75%

Cons

- Accident-and-illness plan cut off at age 15

- There are reports on considerable hikes in renewal premiums, with some users stating that they noticed increases of 50%-90% in chosen instances. These numbers reflect the personal experiences of users and may not represent an average increase for all policies.

- Exam fees and prescription drugs cost extra (most competitors include these)

- An accident-only plan has fixed terms, no customization

- Wellness Rewards not available in Maine, Rhode Island, or Wisconsin

- Dental illness coverage capped at $1,000/year

- First claim triggers full medical history review, adds weeks to processing

- Only 3 discounts vs. competitors offering 4–5

What Does Embrace Actually Cover? (Beyond the Bullet Points)

Most reviews give you a list. I want to give you context, because the difference between what is covered and what actually gets paid is often in the nuance.

Accident & Illness Plan — The Customizable Core

Your pet must be at least 6 weeks old and under 15 years old. You choose your deductible ($100–$1,000), reimbursement rate (70%, 80%, or 90%), and annual limit ($5,000 up to unlimited). One thing most articles skip: your pet needs a vet exam within the 12 months before your policy starts, or within 14 days after. If that does not happen, Embrace automatically defaults your coverage to accident-only. I have seen people not realize this until they filed their first illness claim.

What’s Covered That Competitors Often Miss

Beyond standard accidents and illnesses, Embrace covers:

- Dental illnesses like gingivitis, periodontal disease, abscessed teeth, and endodontic treatment (up to $1,000/year)

- Behavioral therapy, when a licensed vet administers it for a covered condition

- Complementary care, like acupuncture, chiropractic, hydrotherapy, and stem cell therapy for covered conditions

- Euthanasia, for a covered condition or humane reasons unrelated to preexisting conditions

- Mobility devices and prosthetics

- Medical waste disposal

⚠️ Important Limitation: Prescription food is not covered in the standard plan, even if your vet says it’s necessary. Some pet owners only find this out later. To get coverage for it, you need to add the Wellness Rewards option, which costs extra each month.

The Wellness Rewards Program — The Real Differentiator

This is honestly where Embrace stands out from almost everyone. Three tiers: $300, $500, or $700 annually. No deductible. No waiting period. And the coverage list goes well beyond what “wellness” typically means:

- Wearable pet activity monitors and GPS locators

- Dog training: obedience, manners, advanced skills

- End-of-life care: cremation, burial, urns, pawprint keepsakes

- Gastropexy (stomach tacking surgery to prevent bloat)

- Nutritional consultations with your vet

You also get a $25 credit automatically added to your account when you first enroll. No other major insurer in our analysis covers end-of-life keepsake items under wellness

3 Hidden Policy Mechanics That Catch Pet Owners Off Guard

This is the section I wish I had seen before I started looking into pet insurance. These three points are hidden deep in Embrace’s Terms & Conditions and are rarely explained in normal reviews, but they are behind most of the real complaints I came across.

The Bilateral Condition Rule (Bigger Than It Seems)

Embrace explains it like this: “A bilateral condition is a health issue that affects both sides of the body. Because pets have a higher chance of getting the same problem on the other side of the body, if one side is already considered pre-existing, they will not cover the other side later.”

In simple words, if your dog injures one knee before your policy starts, and then injures the other knee after getting coverage, the second claim will likely be denied. This applies to common issues like ligament tears, hip dysplasia, elbow dysplasia, and patellar luxation. And this situation is not rare. Research shows that more than half of dogs who tear one knee ligament end up tearing the other within two years.

What a real user said about this (Golden Retriever Forum, 2024):

“I’m trying to decide if a shorter waiting period is worth the risk. If the vet finds a problem during examination, it could be counted as pre-existing and never be covered. I’m worried about discovering an issue during the exam and then having no insurance support for it in the future.”

Pet Forum User, goldenretrieverforum.com

Source: Golden Retriever Forum

The Orthopedic Exam That Can Backfire

Embrace allows you to shorten your waiting period from 6 months to just 14 days if your vet completes the report card within 14 days. It may sound like a great deal, but there is an important side effect that most people don’t talk about in their reviews.

According to Embrace, if your vet notices any issue during the exam and writes it on your report, that condition and anything related to it, it is most likely to be pre-existing and will not be covered.

So on one side, you are trying to get coverage faster. But on the other side, if your vet finds even a small issue you don’t know about, you may end up permanently losing coverage for that condition.

My opinion: If your dog is a high-risk breed like a German Shepherd, Golden Retriever, or Rottweiler, and is under 2 years old, you should be very careful with this exam. It’s a good idea to talk to your vet first before submitting the report to Embrace.

Upgrading Your Policy Resets Everything

This part sounds like a surprise.

According to Embrace, you can upgrade your plan anytime, but it is treated like starting a completely new policy. That means you will have new waiting periods, and any past health issues that were covered before can now be labeled as pre-existing.

For example, if you upgrade your coverage after a few years, your dog’s previous conditions may no longer be covered under the new terms.

Tip: You should choose your coverage carefully from the start. It is safer to go with the highest limit you can afford early, because changing it later can create problems.

As Dr. Karen Becker explains,

when choosing pet insurance, you should always read how the policy defines “pre-existing condition,” not just rely on marketing. Some policies use broad definitions, where even a small past symptom can later be used to deny a claim. For example, a single recorded episode of vomiting in old records could be used to reject a completely different stomach-related claim years later.

Dr. Karen Becker, DVM

Source: Dr.KarenBecker.com

How Much Does Embrace Really Cost? (Including the Increases)

| Dogs | Cats | |

|---|---|---|

| Sample Monthly Premium | $62.17/mo | $45.84/mo |

| vs. U.S. Average | On par | $10+ above average |

| Ranking in Our Analysis | 2nd lowest | Higher end |

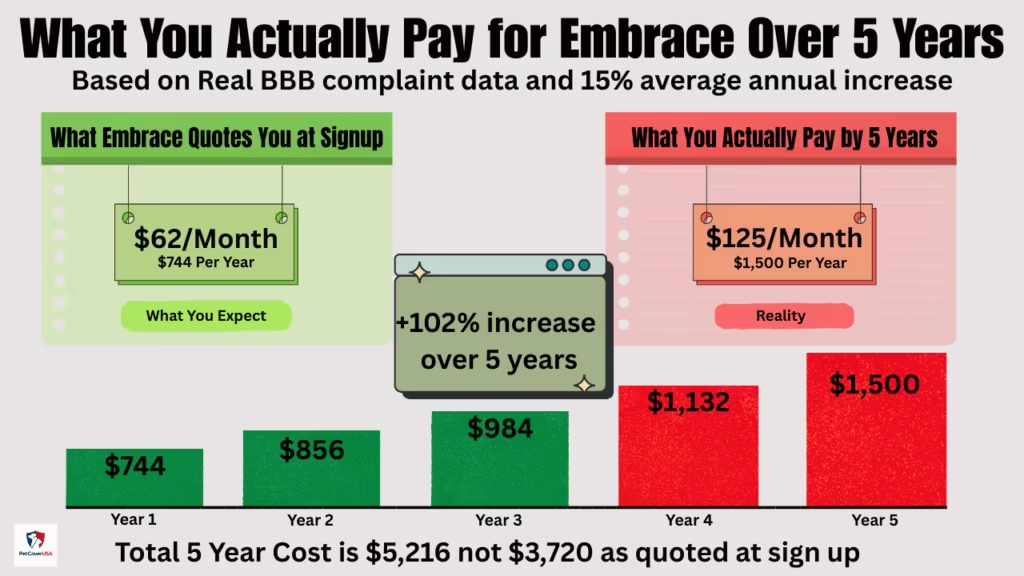

Those headline numbers look reasonable. But here is the data point almost every review buries: premium increases at renewal.

Based on real BBB complaints and ConsumerAffairs reviews I examined, the pattern is consistent:

- One user reported their monthly premium jumped from $98 to $118 after just the first year ( a 20% increase)

- A long-term customer reported their 2025 renewal came in at $757.49/month, up from $449 the prior year

- A third BBB complaint described a renewal that nearly doubled: from $256/month to $493/month within the same policy year

Source: Better Business Bureau — Embrace Pet Insurance Complaints

When asked. Embrace replied that price increases are based on some factors, like your pet’s age, how long you have had the policy, and rising vet costs. This is technically true, but it does not make a high price easier to handle.

Real-world example:

If you start with $52 per month for a 2-year-old dog and the price increases 15% each year, it could reach about $125 pet month by the 5th year and over $200 per month by the 8th year. So plan for future increases, not just the starting price.

The Three Discounts — and How to Stack Them

- Multi-Pet (10%): Applied automatically when your second pet enrolls. Available in all states.

- Military (5%): For active or former U.S. Air Force, Army, Coast Guard, Marines, or Navy. Unavailable in New York and Tennessee.

- Healthy Pet (5–10%): Reimbursed less than $300/year? You qualify for 5% off. Maintain that for two years, and it increases to 10%.

Combined correctly, you can hit the 25% maximum cap — bringing a $62/month premium down to about $46.50/month.

What Real Customers Experience When Filing Claims

In clear words, Embrace works well for simple claims that have no medical history issues. Many users report fast and easy reimbursement, especially for surgeries. One person said they submitted a $7,000 emergency claim within 10 minutes and handled the rest smoothly. But once medical history comes in, things get more complicated.

First claim review:

Embrace does not mention it clearly at sign-up, but your first illness claim triggers a full review of your pet’s medical records from all vets. This process can take more than the usual 10 to 15 days. Some users report delays, repeated document requests, and even claims are denied on the basis of minor issues in medical records in the past.

Trustpilot review (March 2026):

According to a user, Embrace put their claim on hold by saying no records were received, even though the vet had sent them twice. After filing a complaint, the claim was reviewed, but then it was denied because of a minor issue( a food reaction with Vomiting).

Source: www.trustpilot.com

Consumer Affairs review 2024:

According to a user with 25 years in insurance, their cat had a past issue, then later developed a different one. Embrace still denied the claim by saying that it was pre-existing, even though the conditions were not the same.

Appeal window:

If your claim is denied, you have only 14 days to appeal. Your vet must provide a written statement with supporting records. This is a short window, so it’s important to act quickly.

When things are right:

For clear cases with no history of medical issues, claims are often processed quickly. Some users say they receive payments within 1 or 2 weeks, and their app and website are generally easy to use

Deep Research Table: Embrace vs. Pets Best vs. ASPCA

Standard reviews compare prices and deductibles. Here is what actually matters when you are at the vet with a sick animal:

| Category | Embrace | Pets Best | ASPCA |

|---|---|---|---|

| Overall Rating | 4.4 / 5.0 | 4.7 / 5.0 | 4.8 / 5.0 ✅ |

| Sample Monthly — Dog | $62.17 | $47.58 ✅ | $76.78 |

| Sample Monthly — Cat | $45.84 | $29.36 ✅ | $39.20 |

| Age Limit (A&I Plan) | ⚠️ 15 years max | ✅ No limit | ✅ No limit |

| Exam Fees Included? | ⚠️ Add-on cost | Depends on tier | ✅ Included |

| Rx Drug Coverage | ⚠️ Add-on cost | ✅ Included | ✅ Included |

| Curable Preexisting | ✅ 12 months symptom-free | Varies | Limited |

| Bilateral Exclusion | ⚠️ Yes — if prior | ⚠️ Yes | ⚠️ Yes |

| Orthopedic Waiting Period | 6 mo (reducible to 14d) | 6 months | ✅ 14 days |

| Wellness Tiers | ✅ 3 tiers | 2 tiers | 1 tier |

| Wellness Covers Training? | ✅ Yes | ❌ No | ❌ No |

| Wellness End-of-Life Care? | ✅ Yes (cremation, urns) | ❌ No | ❌ No |

| Number of Discounts | 3 (max 25%) | 5 | 3 |

| Coverage Upgrade = Reset? | ⚠️ Yes — full re-underwriting | Varies | Varies |

| Dental Illness Coverage | Up to $1,000/yr | Included | Included |

| Reddit Positive Sentiment | ⚠️ 29% | ~45% | ✅ ~55% |

| Private Equity Owned? | Yes — JAB Holdings | Yes — Poodle Holdings | No — Crum & Forster |

The verdict from this comparison:

- Best price? Pets Best — especially for cats ($16+ cheaper/month than Embrace)

- Best wellness coverage? Embrace — nothing else comes close

- Best claims experience? ASPCA — based on user sentiment data

- Senior pets needing full coverage? Pets Best or ASPCA — Embrace’s 15-year limit is a real problem

Who Should (and Should Not) Buy Embrace

✅ Embrace is the right fit if you…

- Have a young, healthy pet with a clean medical record

- Want unlimited annual coverage on an accident-and-illness plan

- Value the most comprehensive wellness coverage on the market

- Have a breed with genetic risk (covered if no prior symptoms at enrollment)

- Are you a USAA or GEICO member (you may already be getting an Embrace policy)

- Have multiple pets and want the 10% multi-pet discount

- Want 24/7 vet tech access included in your policy

❌ Think twice about Embrace if you…

- Have a senior pet over 12 years old (approaching the 15-year cutoff)

- Have a dog with any prior orthopedic history

- Have a rescue pet with incomplete or unclear medical records

- Need long-term cost predictability on a tight budget

- Live in Maine, Rhode Island, or Wisconsin (no Wellness Rewards)

- Expect to need to adjust coverage levels frequently

- Want prescription drugs and exam fees included without paying extra

🙋 Frequently Asked Questions (FAQs)

Does Embrace cover preexisting conditions? +

Not permanently — but it does something most competitors do not. If your pet has a curable preexisting condition (like an ear infection, undiagnosed vomiting, or a bladder issue), Embrace will reconsider covering it after your pet has been completely symptom-free and treatment-free for 12 consecutive months. Incurable conditions like diabetes, allergies, and orthopedic issues that existed before enrollment are permanently excluded.

What is the bilateral condition exclusion and does it affect my dog? +

It is one of Embrace’s most significant hidden exclusions. If your dog had a knee, hip, or elbow condition on one side of their body before or during the waiting period, Embrace will not cover the same condition on the other side. This disproportionately affects large breeds prone to cruciate tears and hip dysplasia. Ask an Embrace representative directly how this applies to your specific dog before purchasing.

How long does Embrace take to reimburse a claim? +

Officially: 10–15 business days for standard claims, 5 business days for wellness claims. Your first claim will typically take longer because Embrace requests your pet’s complete medical history before processing. Direct deposit adds 3 business days; paper check adds around 10 business days.

Will Embrace’s premiums increase every year? +

Yes. Annual increases of 15–25% are common based on real customer reports from BBB and ConsumerAffairs. Some long-term customers have reported much steeper jumps. Budget conservatively — your year-one premium is not your year-five premium.

Is the orthopedic waiting period reduction worth it? +

It depends on your dog’s breed and history. For low-risk, young, mixed-breed dogs the exam is usually worth taking. For high-risk breeds like German Shepherds, Golden Retrievers, or Labs, have a frank conversation with your vet privately before scheduling the exam — because any abnormality noted becomes a permanent exclusion.

Can I use Embrace with any vet? +

Yes — any licensed veterinarian in all 50 states and Washington D.C., including specialists and emergency vets. No network restrictions. Your pet is even covered for up to 6 months of international travel. The one exception: Embrace will not cover treatment performed by a vet who is also the policyholder.

Who actually underwrites Embrace policies? +

Embrace’s policies are underwritten by American Modern Insurance Group, a Munich Re company. Embrace itself was acquired by JAB Holding Company in late 2023 for $1.5 billion. JAB now owns over 21 pet insurance brands globally.

Bottom Line: Is Embrace Worth It in 2026?

After researching hundreds of real experiences, my conclusion is that Embrace works as it is designed. Certain aspects of the agreement may be confusing (like bilateral exclusions and re-underwriting after the upgrade), so it’s essential to read the complete documents carefully.

If your pet is healthy and you understand things like bilateral conditions, the re-underwriting rule for upgrades, and the orthopedic exam risk before buying, then Embrace is a strong choice. It has great wellness coverage, the customization options really work, and Munich Re’s back support makes it financially stable.

But if you have a rescued pet or a senior dog or a history of orthopedic problems, then you should read the fine print carefully first so you can make the right decision.

You should take a screenshot of your deductible, reimbursement rate, and coverage limits on the day you are buying the policy. Then you should check your renewal documents to make sure that they match, and you should call right away in case they don’t match.

Final Recommendation.

Embrace works best for healthy pets younger than 10 years old, as their owners wish to receive unlimited annual coverage and good wellness add-ons. Owners of senior pets or pets with a history of medical conditions should also consider comparing other providers. Before you decide to buy Embrace, you should compare it with Pets Best, which offers better pricing and no age limit.

Trusted External Resources

Our content is supported by information from established organizations and public educational sources to ensure accuracy and transparency.

-

ASPCA – Pet Insurance & Veterinary Care Guide

Nonprofit animal welfare organization offering educational resources for pet owners. -

American Veterinary Medical Association (AVMA)

Official U.S. veterinary association providing professional guidance on pet healthcare. -

U.S. Food & Drug Administration – Animal & Veterinary

Government resource for veterinary medicine safety and regulations. -

North American Pet Health Insurance Association (NAPHIA)

Official industry body publishing annual pet insurance market data and statistics. -

Better Business Bureau – Embrace Pet Insurance Profile

Independent nonprofit organization tracking business complaints and customer reviews. -

Federal Trade Commission (FTC) – Endorsement & Review Guidelines

U.S. government guidelines ensuring transparency in online reviews and recommendations.

External references are included for informational purposes to support accuracy and research quality.

Related Pet Insurance Guides

Before you decide on Embrace, these guides will help you compare your options, understand policy gaps, and choose the right plan for your pet’s specific needs.

-

Embrace Pet Insurance for Older Dogs with Dental Coverage

If your dog is over 8 years old, Embrace’s rules change significantly. This guide covers exactly what dental and senior coverage you actually get — and what gets quietly excluded.

-

What Pet Insurance Actually Covers Pre-Existing Conditions?

Embrace’s preexisting condition policy is one of its most misunderstood areas. This guide breaks down which U.S. insurers are most lenient — and how to avoid a claim denial before you even enroll.

-

Pet Insurance With No Waiting Period in the USA

Embrace has a 6-month orthopedic waiting period that catches many buyers off guard. If you need coverage faster, here are the plans that offer immediate or drastically reduced waiting periods.

-

Pet Insurance for Senior Dogs Over 10 Years Old

Embrace cuts off accident-and-illness coverage at age 15 — but problems start much earlier for senior dogs. This guide covers which insurers genuinely support aging pets without quietly raising your premiums or shrinking your coverage.

-

Best Pet Insurance for Older Dogs: Side-by-Side Comparison 2026

We compared Embrace directly against 6 other insurers on age limits, premium increases, and chronic condition coverage. If your dog is over 7, this comparison will likely change your decision.

-

Pet Insurance That Covers Everything in 2026: What’s Real vs. Marketing

Embrace advertises “unlimited annual coverage” — but unlimited does not mean everything. This guide explains what complete coverage actually looks like, what every insurer quietly excludes, and which plan comes closest to true full coverage.

All guides are independently researched and regularly updated with verified data.

📅 Last Updated:

About the Author

M. Nouman is an independent researcher and writer focused on U.S. pet insurance. He reviews insurer policy documents, coverage terms, waiting periods, reimbursement options, exclusions, and publicly available veterinary and regulatory resources to create clear, research-based guides. His goal is to simplify complex insurance information so pet owners can make informed decisions based on reliable sources rather than marketing claims. Articles are reviewed and updated as policies and industry information change.

Areas of Research: Pet Insurance Policies, Coverage Analysis, Policy Comparisons, Waiting Periods, Reimbursement Models, Policy Exclusions, Claims Education

Research insights and updates on Quora, LinkedIn, and Reddit.