Some links may be affiliate links. We may earn a small commission at no extra cost to you.

Information may change over time and should be verified with official providers. We are not responsible for any decisions made based on this content.

Pet Insurance With No Waiting Period in USA: The Complete 2026 Guide (What Nobody Tells You)

The short answer: true, no-waiting-period pet insurance in the U.S. doesn’t exist for illnesses. But there are some strategies that can be helpful to reduce your waiting period to zero days, as little as 14 days for illness. After my research on 20+ insurers, policy documents, and real user experiences, what I found is that most people did not get caught by the waiting period itself, but what happens during and right after it.

This guide tells exactly how to avoid it

Why I Wrote This (And Why It’s Different From Every Other Blog)

After doing deep research on policy fine prints, reviewing real user experiences on Reddit’s r/petinsurance, and after reviewing data from NAPHIA, AAHA, and Insurify, I kept hitting the same wall.

Most blogs out there tell you what a waiting period is, but almost none of them explain how you can reduce it legally, what becomes the reason for a claim denial after your waiting period is over, and what is hidden in your policy document that most of the insurance industry does not highlight in their marketing pages.

So I put this together for you, whether you just brought home a new puppy, adopted a rescue dog, or watched a friend pay $6,000 out of pocket because their coverage wasn’t what they thought it was. Let me save you that pain.

What Is a Pet Insurance Waiting Period? (And Why It Actually Exists)

A waiting period is a gap between the day you sign up for pet insurance and the day when your coverage actually starts. During this period, if your pet gets sick or injured, you will be paying 100% out of pocket. And here is a thing that really hurts: anything that happens during this waiting period can be permanently flagged as a pre-existing condition, which means that it may never be covered for the life of your policy.

Most blogs stop at “waiting periods prevent fraud.” That’s true, but incomplete. The deeper reason is something Dr. Ricky Walther, DVM — Chief Medical Officer at Pawlicy Advisor and a practicing small animal vet in Sacramento — explained clearly to AAHA in 2025:

“It’s a way to hedge risk. But it’s also not car insurance because your pet has an emotional value to owners, so we are using a product that is property and casualty insurance to cover risk and mitigation for pets that we care about.”

Dr. Ricky Walther, DVM

Source: AAHA (Insights on Pet Insurance in 2025)

This quote is more valuable than it seems. You are not buying any human-type health insurance. You are buying a financial risk hedge for a family member that can’t be replaced emotionally. Once you understand that, the whole structure of waiting periods and how to navigate them makes a lot more sense.

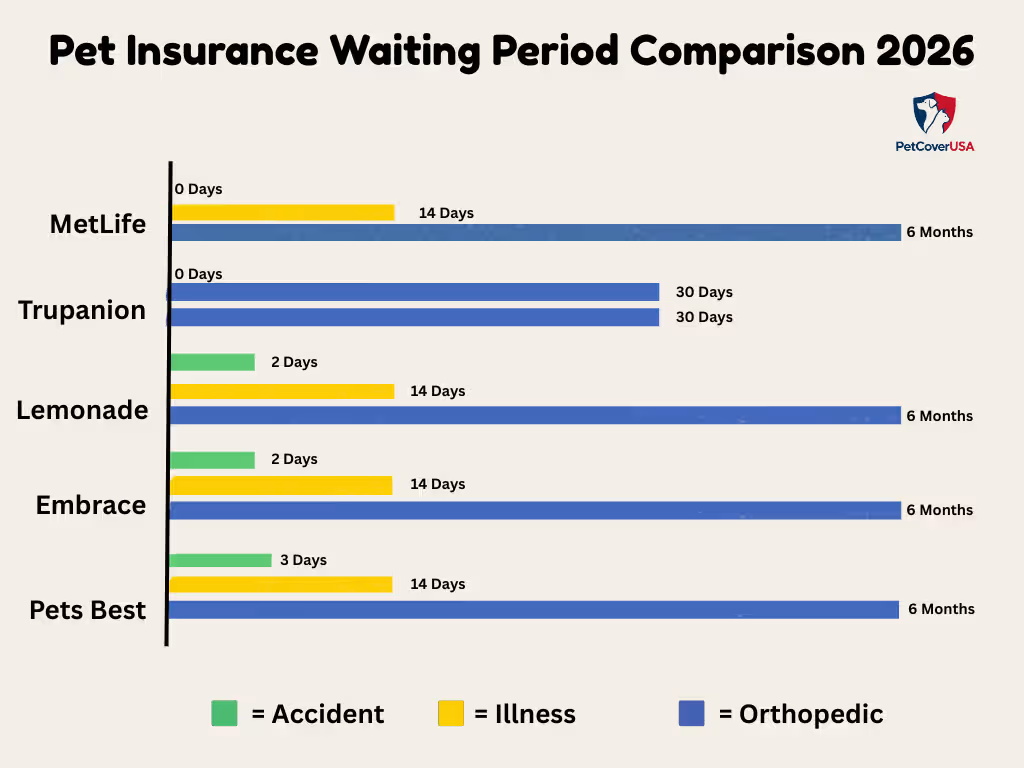

The Real Waiting Period Breakdown in 2026

Here’s what I found when I compared actual policy documents across major US carriers. This includes their actual policy terms, not their marketing pages,

| Coverage Type | Typical Waiting Period | Shortest Available | Key Notes |

|---|---|---|---|

| Accidents | 1–14 days | 0 days (MetLife, Embrace) | Most important to minimize |

| Illnesses | 14–30 days | 14 days (most carriers) | Industry standard |

| Orthopedic conditions | 6–12 months | 14 days (with vet exam waiver) | The biggest hidden trap |

| Preventive/Wellness | 0–14 days | 0 days (ASPCA, Lemonade add-on) | Usually starts next day |

| Hip dysplasia | 12 months | 12 months (Healthy Paws) | Only for pets enrolled under age 6 |

One thing that you should be concerned about is the orthopedic waiting period. Your Labrador, German Shepherd, or French Bulldogs are breeds that are statically prone to joint problems, and can face up to a 12-month waiting period for orthopedic coverage with some insurers. At the same time, cruciate ligament surgery often costs $4,000–$8,000 and is one of the most common claims in the industry.

That gap isn’t a coincidence.

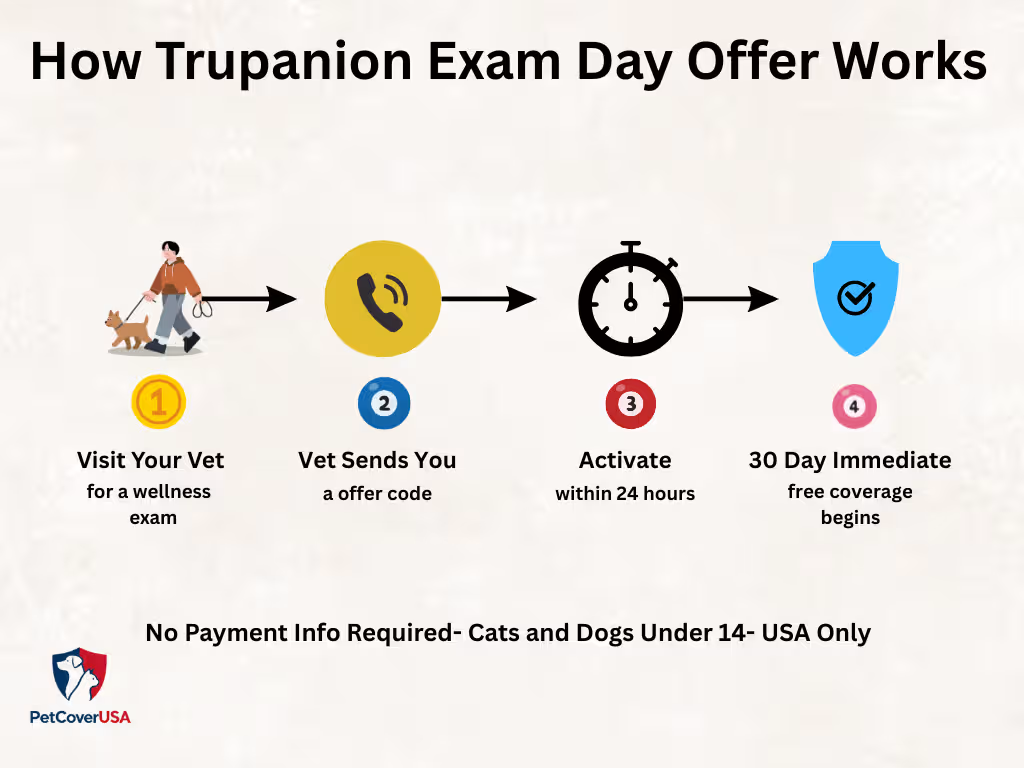

The Trupanion Exam Day Offer: Same-Day Coverage Most People Never Hear About

I want to spend real time on this because I was genuinely surprised that barely any review blogs cover it properly.

Trupanion has a program called the Exam Day Offer, available through participating vet clinics. Here is exactly how it works:

If your vet is part of Trupanion’s network, they can send you a special offer code during your pet’s exam. You need to activate that code within 24 hours of leaving the clinic. Once activated, you get 30 days of full Trupanion coverage with no waiting period, no upfront payment, and no credit card required.

What you actually get during those 30 days:

- 90% reimbursement on new, unexpected injuries and illnesses

- No cap on what Trupanion pays per condition for the life of the policy if you continue

- Get access to any licensed vet in the US, Canada, or Puerto Rico

After 30 days, you can decide whether you want to continue as a paying member. If you don’t want it, your coverage cancels automatically, and you are charged nothing.

Trupanion also offers a similar “Go Home Day Offer” for newly adopted pets, which activates within 24 hours before or after your adoption date with the same structure and benefits.

Your cat or dog should be under 14 years for eligibility.

Source: Trupanion Exam Day Offer FAQ

According to Trupaio’s vet program documents, ” Coverage begins once the offer is activated and must be activated within 24 hours after the exam.”

Source: Trupanion Exam Day Offer — Vet FAQ

In my opinion: If you have a routine vet visit coming up, you should call ahead and ask whether you clinic participates in Trupanion’s Exam Day Offer program. It takes 30 seconds to ask and could give you 30 days of real coverage while you compare plans. This is the closest thing to genuinely free, instant pet insurance in the US market right now.

4 Legitimate Ways to Minimize or Skip Your Waiting Period

Get a Vet Exam Waiver for Orthopedic Coverage

This single step can save you months of going without coverage for your pet’s most expensive injuries. Several major injuries will reduce the orthopedic waiting period from 6 months all the way down to 14 days, but only if you submit a vet exam form within a specific period around your policy start date.

Here’s what each carrier requires:

- Pets Best: Vet exam must happen 3 days before or 7 days after your policy’s effective date. Submit the form within 30 days.

- Embrace: An orthopedic exam reduces the wait from 6 months to 14 days.

- Fetch: Hip and knee waiting period is waived if a vet exam is completed within 30 days of enrollment and your pet is cleared.

Source: Pets Best FAQ

Source: NerdWallet, Pet Insurance Waiting Periods

The problem is that insurance companies don’t tell this clearly. When you buy a policy, ask the insurer directly:” Do you have a waiting period waiver form, and what is the deadline?” Most reps won’t bring it up unless you do.

Switch Providers and Use the ManyPets Switcher Offer

ManyPets offers one of the few real ways to reduce the waiting period for illness in the U.S. If you switch from an active pet insurance policy to ManyPets and your previous coverage was still active within 24 hours of your new policy start date, the illness waiting period can be fully waived.

You’ll need documents that show that your policy was active. Call ManyPets before canceling your old policy to confirm exactly what they need.

Source: Insurify (Best Pet Insurance With No Waiting Period)

Important caveat: ManyPets does not waive the waiting period for hip dysplasia, cruciate ligament conditions, or IVDD. These conditions usually have separate, longer waiting periods and are not included in waiting period waivers, even when you switch policies.

Access MetLife Pet Through Your Employer (Pre-Existing Condition Transfer)

This is one of the most overlooked but valuable details I found in my research.

MetLife Pet Insurance, when you access MetLife Pet Insurance through an employer benefit plan, it may allow certain pre-existing conditions to carry over if they were already covered under your previous policy.

That means if your current insurer covers conditions like allergies, chronic ear infections, or diabetes, and you switch to MetLife Pet Insurance through your employer, that coverage can transfer.

This kind of carryover is extremely rare in the U.S. pet insurance market and is not available if you try to enroll through MetLife’s website. It is only available through eligible employer plans.

Source: MetLife Pet Pre-Existing Conditions

If you are changing jobs, it is better to ask your HR team whether MetLife Pet is offered before you make any decision.

Adopt From a Participating Shelter and Use Fetch’s Day-One Coverage

Currently, Fetch Pet Insurance is the only U.S insurer that covers Common pre-existing conditions from day one for pets who are newly adopted from participating shelters and rescues. If your newly adopted dog has a prior diagnosis on the record, Fetch may cover it from your enrollment date, not after a waiting period.

Source: Fetch Pet Insurance

This does not apply to all conditions or all shelters, so you should confirm with Fetch directly. But for rescue adopters, it is better to ask before choosing an insurer.

The Pre-Existing Condition Traps Nobody Warns You About

The Symptom Problem (This One Gets People Every Time)

Pet insurance companies don’t only look at your normal diagnosis files; instead, they check your pet’s complete vet record history to find out any documented symptoms like limping, scratching, digestive issues, eye discharge that could connect to your current claim.

From ASPCA Pet Insurance’s own policy language:

“Conditions that have not been diagnosed or treated yet can still be considered pre-existing. For instance, say your dog starts limping in March before you sign up for pet insurance… if you enroll in pet insurance in April, and your dog starts limping again, then any necessary future treatments related to this issue will not be covered.”

ASPCA Pet Insurance

Source: ASPCA Pet Insurance Pre-Existing Conditions

So, before you enroll anywhere, get a copy of your pet’s complete vet record and read it yourself carefully. Look for symptoms that could later be used as a reason to deny a claim. If you find anything, factor it into your carrier decision, because different carriers define pre-existing conditions differently, and some are more lenient than others.

The Bilateral Condition Rule

Here is something that I genuinely could ot find in any other major blog explained properly.

If your dog had a cruciate ligament injury in the left knee before your policy started, Many insurance companies will deny the right knee claim in the future, even though the right knee was never injured. This is called a bilateral condition exclusion

It is because research shows that 40-60% dogs that tear the cruciate ligament will tear the other leg too after one month, one year, or later. Insurers treat the healthy knee as a connected risk to the previously injured one. This exclusion applies to most major carriers, including Embrace, ASPCA, and Lemonade.

MetLife Pet is the one company that will cover bilateral conditions as long as your pet’s records don’t show that one side was previously affected.

Source: MetLife Pet Pre-Existing Conditions

Source: Money.com Pet Insurance Claim Denied

The Cancel-and-Rejoin Trap

If you cancel your policy and then try to enroll in a new insurance company or the same old insurance company, your waiting period resets fully. Every condition your pet developed during your previous policy is now a pre-existing condition for your new policy.

Lemonade is one of the few carriers honest enough to say this clearly in their own FAQ:

“If you were to cancel and reapply for Lemonade Pet again down the line, the waiting periods would reset, potentially expanding the list of illnesses and conditions that would be considered pre-existing.”

Lemonade Pet Insurance

Source: Lemonade Pet Claim Denials

The lesson: once you’ve passed your waiting period with any carrier, that history is an asset. Don’t throw it away unless you have a compelling strategic reason to switch.

Deep Research Comparison: MetLife Pet vs. Lemonade vs. Trupanion

I chose these three specifically because they represent the three most distinct approaches to waiting periods in the current US market.

| Feature | MetLife Pet | Lemonade Pet | Trupanion |

|---|---|---|---|

| Accident waiting period | 0 days | 2 days | 0 days (Exam Day Offer only) |

| Illness waiting period | 14 days | 14 days | 0 days (Exam Day Offer only) |

| Orthopedic waiting period | 14 days (no separate period) | 30 days | 30 days |

| Orthopedic waiver option | Not needed | No | No (Exam Day bypasses all) |

| Pre-existing condition transfer | Yes (employer plans only) | No | No |

| Bilateral conditions covered | Yes (if one side not previously affected) | No | No |

| Average monthly cost — dog (2026) | ~$52 | ~$35–55 | ~$60–90 |

| Reimbursement percentage | 50–90% (your choice) | 70–90% (your choice) | 90% flat (no choice) |

| Annual payout cap | Flexible limit you choose | Flexible limit you choose | Unlimited |

| Same-day activation option | No (retail) | No | Yes (via vet Exam Day Offer) |

| Preventive care waiting period | 0 days | 0 days (starts next day) | Not included in base policy |

| Cancel-and-rejoin penalty | Waiting period resets | Waiting period resets + new pre-existing list | Waiting period resets |

Sources: MetLife Pet, Lemonade, and Trupanion

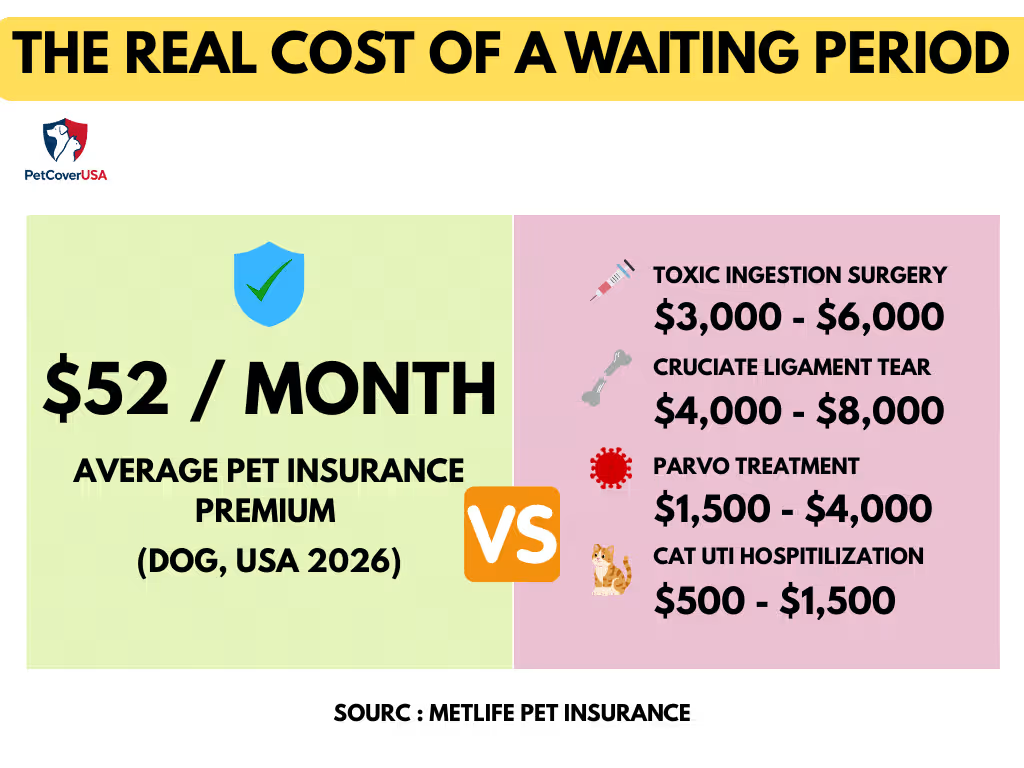

What You’re Actually Risking During a Waiting Period (In Real Numbers)

“You will pay out of pocket” doesn’t mean much on its own. Here’s what it actually looks like in numbers.

According to data from MetLife Pet Insurance in 2026, an emergency vet visit for a dog can cost up to $5,000 or more, and for cats, it may be up to $3000 or more.

Source: MetLife Pet, How Much Does Pet Insurance Cost 2026

The average monthly premium in 2026 is approximately $52 for dogs and $28 for cats nationally.

Source: MetLife Pet 2026 Cost Data

Here’s what that 14-day illness waiting period actually means in financial exposure:

| What happens during your wait | Your cost if uninsured | What you’d recover at 80% reimbursement after wait |

|---|---|---|

| Dog eats something toxic (surgery) | $3,000–$6,000 | $2,400–$4,800 covered |

| Cat UTI with hospitalization | $500–$1,500 | $400–$1,200 covered |

| Dog cruciate ligament tear | $4,000–$8,000 | $3,200–$6,400 covered |

| Puppy parvovirus treatment | $1,500–$4,000 | $1,200–$3,200 covered |

This risk is highest for the pets that usually go the longest without insurance. Trupanion’s internal data shows that 1 in 2 puppies experiences an unexpected injury or illness in their first year.

Source: Trupanion Exam Day Offer FAQ

The 180-Day Pre-Existing Condition Reset: How to Use It in Your Favor

In my opinion, here is something that can actually work for you, and almost nobody talks about it.

Several major insurance companies will remove a pre-existing condition exclusion if your pet stays symptom-free and treatment-free for a certain period after you enroll. In simple words, a condition that your pet had appeared before signing up for a policy could become covered, if it does not appear during a certain period of time.

| Carrier | Reset Period | What Never Resets |

|---|---|---|

| ASPCA | 180 days symptom + treatment-free | Knee/ligament conditions |

| Spot Pet Insurance | 180 days | Knee/ligament conditions |

| ManyPets | 18 months | Hip dysplasia, cruciate, IVDD |

| Figo | 12 months | Cancer, bone/joint, diabetes, allergies |

| USAA (Embrace underwriting) | 12 months | Standard exclusions apply |

Sources: ASPCA Pet Insurance, ManyPets, and Best Money.

If your dog had an ear infection or respiratory infection and had recovered before enrolling in an insurance policy, then you should go for a policy that has a 180-day reset period. You should have a track of 180 days after your insurance starts.

If your pet does not repeat the same symptoms or treatment within this duration, then that condition could be eligible to be recovered from again. This is not a trick or cheating; this is how policies are designed. But most people don’t know about it.

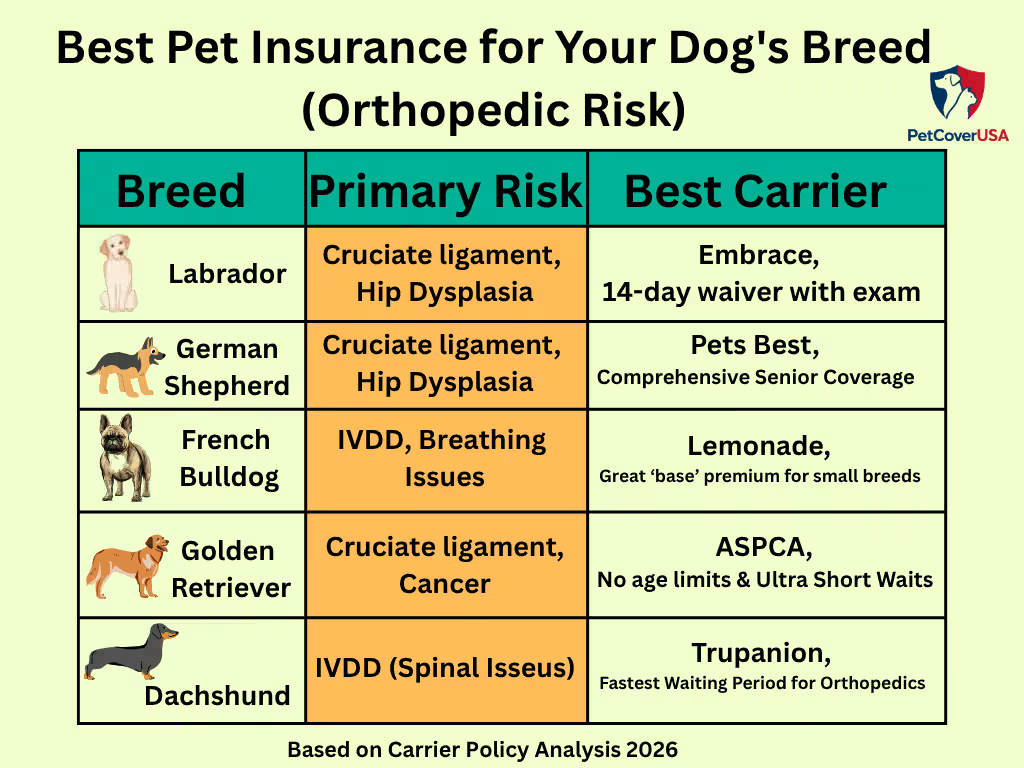

Which Breeds Need the Shortest Orthopedic Waiting Period (And Which Carrier to Choose)

This is a gap I noticed while comparing many blogs: your pet’s breed should directly influence the insurance provider you choose, specifically around the orthopedic coverage timeline. Nobody explained this to you. Here it is.

| Breed | Primary orthopedic risk | Average treatment cost | Best carrier for ortho wait |

|---|---|---|---|

| Labrador Retriever | Cruciate ligament, hip dysplasia | $4,000–$7,000 | Embrace (14-day waiver with exam) |

| German Shepherd | Hip and elbow dysplasia | $3,500–$6,000 | Embrace or Pets Best (waiver available) |

| French Bulldog | IVDD, patellar luxation | $3,000–$8,000 | MetLife (no separate ortho period) |

| Golden Retriever | Cruciate, hip dysplasia | $4,000–$7,500 | Embrace (14-day waiver with exam) |

| Dachshund | IVDD | $2,500–$5,000 | MetLife (no separate ortho period) |

MetLife Pet wins here because it doesn’t have a separate orthopedic waiting period at all; orthopedic conditions fall under the standard 14-day illness period. For high-risk breeds, this is a real advantage compared to plans that have a separate 6-month waiting period for orthopedic conditions.

Source: NerdWallet, Pet Insurance Waiting Periods

When “No Waiting Period” Doesn’t Mean What You Think

This phrase is used in such a way during marketing that it can totally mislead you. Here is a breakdown in simple language:

“Coverage starts the day after enrollment.”

This is typically true only for accidents, not for illnesses. Always ask your insurer what it means for your illness waiting period specifically.

“Immediate coverage available”

It usually refers to Trupanion’s Exam Day Offer or wellness add-ons. Your core accident and illness insurance policy still has a standard wait.

“No waiting period for preventive care”

It is accurate for most carriers, but preventive care (annual exams, vaccines) is a small fraction of what you’d actually claim. The real money is in accidents and illnesses.

“Zero-day waiting period”

MetLife’s 0-day accident coverage is legitimate and verifiable. Illness still has a 14-day wait.

My rule whenever you read a marketing advertisement: you should ask three separate questions: what is my waiting period for accident, what is my illness waiting period, and what is my orthopedic waiting period? They almost always have three different answers.

❓ FAQs About Pet Insurance With No Waiting Period in USA

Can I get pet insurance with absolutely no waiting period for illnesses?

What will happen if my pet gets sick during the waiting period?

Will the waiting period reset when I renew my policy?

Source: NerdWallet — https://www.nerdwallet.com/insurance/pet/learn/pet-insurance-waiting-periods

Is accident-only coverage a good workaround for the waiting period?

Can I have two pet insurance policies at the same time?

What’s the fastest legitimate way to get full coverage right now?

My Final Take

After my research on all policy documents, insurance provider comparisons, real user research, vet data, here is what I’d tell a close friend.

You should get your pet insured on the day you bring your pet home. Not after a week, not after the first vet visit. I would advise you to get your pet insured the day you bring it home. Every day you wait is a day during which any symptom that appears becomes potentially uninsurable for years.

If you have a vet appointment coming up, before you leave the clinic, ask your vet about the Trupanion Exam Day Offer. It’s the only way to get genuine same-day coverage in the US right now, and it costs you nothing to try.

If you have a high-risk breed, like a Labrador, French Bulldog, or German Shepherd, then prioritize an insurer that provides a shorter orthopedic waiting period or has waiver options available.

If you save $10 per month from a plan but it doesn’t cover an $8,000 surgery, and it’s because you chose the wrong plan, then these savings have no practical value.

I would advise you that whatever you do, never cancel and re-enroll in the policy. That is the most expensive mistake in the pet insurance industry, and the easiest one to avoid.

The U.S. pet insurance market has generated over $4.7 billion in gross written premiums in 2024, a 21.4% increase from 2023, which is yet fewer than 4% of pet owners in the U.S. are actually insured. That gap exists largely because most people don’t know where to start or don’t understand what the fine print really means.

Now you do.

Sources: Lancaster Puppies, 6 Key US Pet Insurance Statistics 2025

AAHA Pet Insurance Insights 2025

Information on this page is based on publicly available policy details, insurer documentation, and general research as of the time of writing. Coverage terms, waiting periods, and pricing may vary by provider and can change over time. Readers should confirm the latest policy details directly with the insurance provider before making any decision.

Related Pet Insurance Guides

Best Pet Insurance That Covers Dental for Dogs

Explore detailed dental coverage options for dogs and learn how top U.S. pet insurance plans handle cleanings, extractions, and oral care.

Affordable Pet Insurance Plans for Dogs and Cats 2026

Compare budget-friendly insurance plans for both dogs and cats, without compromising on critical health coverage and financial protection.

Is Pet Insurance Worth It for First-Time Pet Owners?

A practical guide for new pet parents weighing the costs, benefits, and potential pitfalls of investing in pet insurance from day one.

Pet Insurance for Senior Dogs Over 10 Years Old

Senior dogs need specialized coverage; discover plans that handle chronic conditions, age-related illnesses, and emergencies for older pets.

Lemonade Pet Insurance Review 2026 – Worth It or Not

A comprehensive review of Lemonade pet insurance, evaluating pricing, claim speed, and real-world coverage for both healthy and aging pets.

Embrace Pet Insurance Review 2026 – Worth It or Not

Detailed insights on Embrace policies for chronic conditions, dental care, and preventive coverage to make informed decisions for your pets.

📅 Last Updated:

About the Author

M. Nouman is an independent researcher and writer focused on U.S. pet insurance. He reviews insurer policy documents, coverage terms, waiting periods, reimbursement options, exclusions, and publicly available veterinary and regulatory resources to create clear, research-based guides. His goal is to simplify complex insurance information so pet owners can make informed decisions based on reliable sources rather than marketing claims. Articles are reviewed and updated as policies and industry information change.

Areas of Research: Pet Insurance Policies, Coverage Analysis, Policy Comparisons, Waiting Periods, Reimbursement Models, Policy Exclusions, Claims Education

Research insights and updates on Quora, LinkedIn, and Reddit.