Some links may be affiliate links. We may earn a small commission at no extra cost to you.

Information may change over time and should be verified with official providers. We are not responsible for any decisions made based on this content.

Pet Insurance That Covers Everything: What You Actually Get (And the Gaps Nobody Warns You About)

The short answer to this question is no pet insurance plan literally covers everything, but a few things, like a comprehensive plan, chosen at the right time, can cover 80-90% of vet bills. The difference between a plan that works and one that fails you comes with the five common wrong decisions most pet owners make.

I have spent weeks researching 19+ pet insurance companies, digging through real claim denial stories on Reddit and pet owner forums, analyzing NAPHIA’s 2025 state of industry report, and cross-referencing policy documents side by side. What I found in my research will shock you. Most content tells you what pet insurance covers, but almost nobody tells you what things cause your claim to be denied after you have paid premiums for years. And in this blog, I’ll tell you how you can fix this.

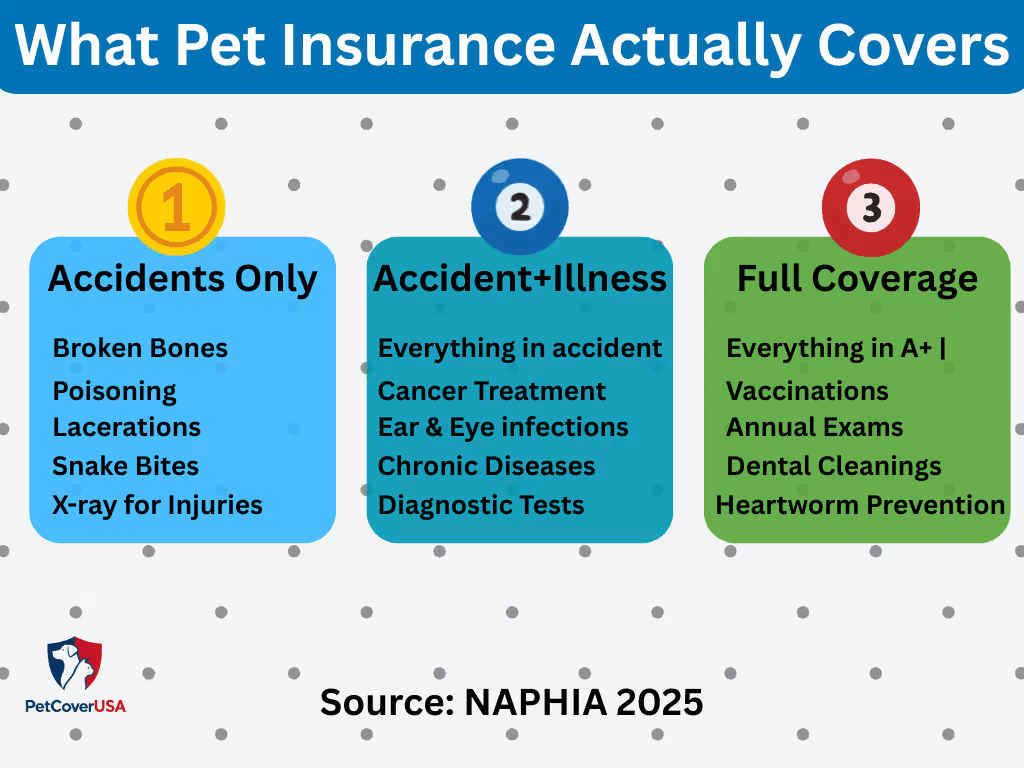

What Does “Full Coverage” Pet Insurance Actually Mean?

I’ll be clear: when you see “comprehensive” or “full coverage” in pet insurance, it usually means accident + illness + optional wellness. It does not mean everything.

Here is the breakdown that matters:

The Three Plan Types — Which One Do You Actually Need?

| Plan Type | What It Covers | Best For | Avg. Monthly Cost (Dog) |

|---|---|---|---|

| Accident-Only | Broken bones, swallowed objects, lacerations, poisoning | Tight budgets, healthy young pets | $15–$30 |

| Accident + Illness | Everything above + cancer, diabetes, infections, hereditary conditions | Most pet owners — best value | $37–$73 |

| Accident + Illness + Wellness | Everything above + vaccines, annual exams, dental cleanings | Owners who use all preventive care benefits | $70–$120+ |

Source: Pawlicy Advisor. (March 2026 median data from thousands of real customer quotes)

During my research, I noticed that accident + illness plans are where about 85% of all pet insurance claims happen, because illnesses like cancer, diabetes, and kidney disease create the biggest bills, not accidents.

“Modern veterinary treatments — stem cell transplants, open-heart surgery, advanced oncology — are now available to pets. Without insurance, most families can’t access them.”

Dr. Karen Halligan, DVM, host of Collars and Cents

Source: Money.com, April 2026

What a Truly Comprehensive Pet Insurance Plan Covers

Based on my research and by reviewing top- rated providers, here’s what the best plans include in 2026:

Always covered in top-tier accident + illness plans:

- Emergency surgeries and hospitalizations (including overnight stays)

- Cancer diagnosis and treatment (chemotherapy, radiation, surgery)

- Hereditary and congenital conditions (hip dysplasia, IVDD, heart defects) — when not pre-existing

- Chronic conditions (diabetes, arthritis, epilepsy), with no per-condition limits in the best plans

- Diagnostic testing (MRI, X-rays, biopsies, bloodwork)

- Specialist visits (oncologists, neurologists, cardiologists)

- Prescription medications

- Dental illness, like extractions, periodontal disease, gingivitis (up to $1,000/year with Embrace)

- Alternative therapies like acupuncture, laser therapy, hydrotherapy

Covered by some providers, not all:

- Behavioral therapy (ASPCA, Spot, MetLife -yes; many others -no)

- Exam fees (MetLife, Figo with opt-in – yes; most standard plans – no)

- Prescription food (ASPCA, Trupanion for covered conditions – yes; most -no)

- Microchipping (ASPCA – yes; most- no)

Source: NerdWallet pet insurance analysis, 2026

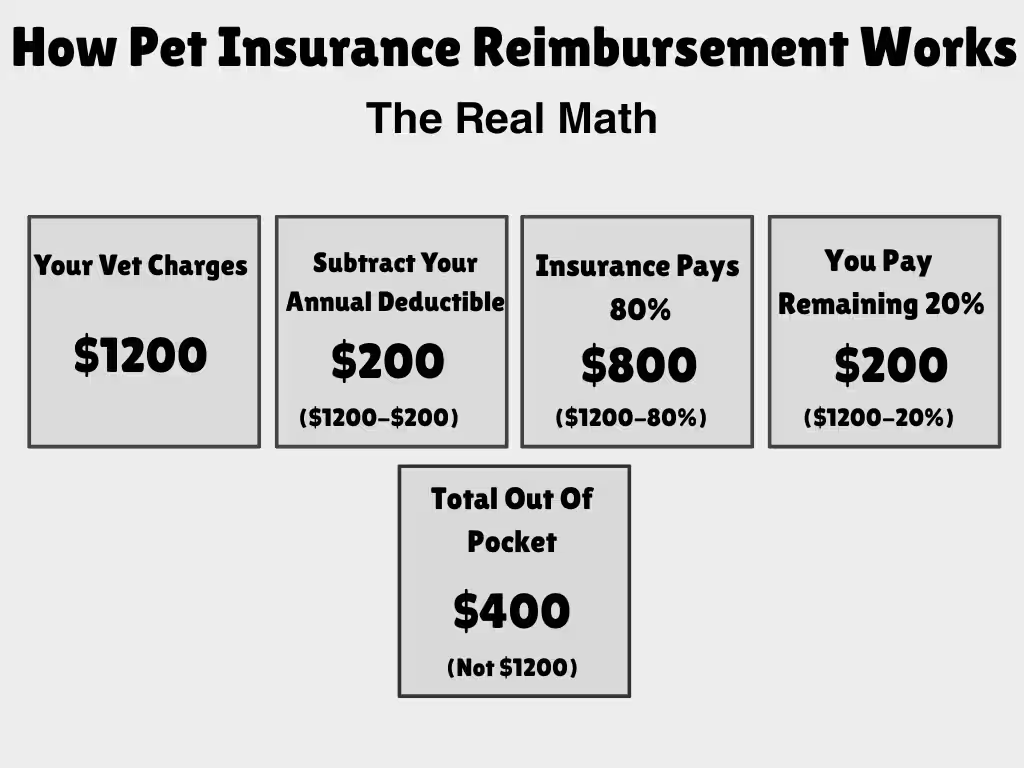

The “80% Reimbursement” Illusion ( Read This Before You Buy Anything)

During my research, I was genuinely surprised by something, and it barely gets mentioned anywhere.

When a policy says “80% reimbursment,” you probably think that insurance pays $800 out of $1000 vet bills. Sometimes that’s exactly right. Sometimes your actual payout is $190 on an $800 bill. Here’s why.

The Three Reimbursement Methods (And Which One Actually Pays You Fairly)

Method 1: Percentage of Actual Vet Bill

This is the best and most transparent method used by Lemonade, Healthy Paws, Embrace, ASPCA, Figo, Pets Best. Example: If your vet bill is $1,200, first subtract the $200 deductible, leaving $1,000. You get 80% of that back, which is $800.

Method 2: Benefit Schedule

This method was used by some Nationwide plans historically. The insurer has an internal price list for every procedure. If your vet charges more than their list price, they pay only their listed amount, not yours. For example, if your vet charges $800 for a procedure but your plan caps that treatment at $300, you’ll only get $300 back, not $640. In high-cost cities, where vet fees are much higher than average, this gap can become significant.

Method 3: “Copay Then Deductible” vs. “Deductible Then Copay”

Even in percentage-based plans, the order of calculation matters.

- Deductible first: From a $1,200 bill, subtract $200 → $1,000 left → 80% back = $800

- Copay first: From $1,200, take 80% = $960 → then subtract $200 → $760 back

That’s a $40 difference on a small bill — and $400+ on a $10,000 surgery.

Source: Embrace Pet Insurance reimbursement breakdown

My advice: always ask the insurer, “Do you reimburse based on my actual vet bill or a set price list?” If they can’t give you a clear answer, don’t choose that Company

The Hidden Gaps That Cost Pet Owners Thousands, And Nobody Talks About

This is important to understand carefully because this is where many pet owners end up losing thousands of dollars each year, and most comparison sites don’t explain it.

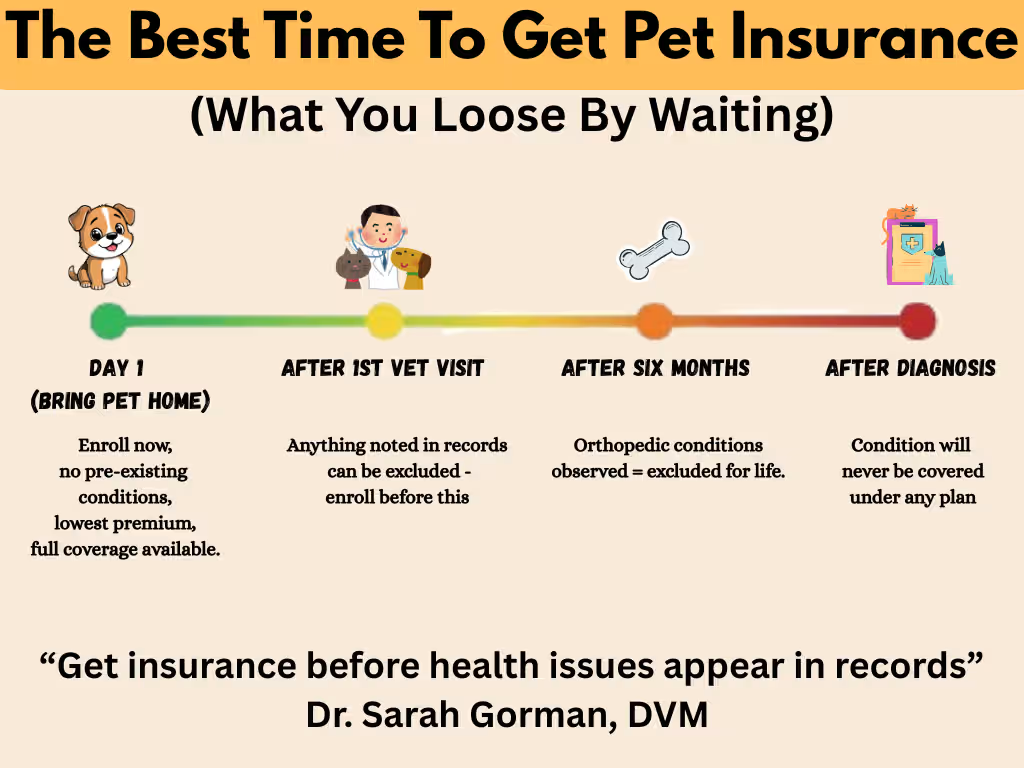

Your Vet’s Notes Can Kill a Future Claim Before You Even Apply

The scenario I found repeated across multiple owner communities is that a dog goes to the vet for a routine puppy checkup. The vet casually writes in the chart, “Owner reports occasional limping.” No diagnosis. No treatment. Just a note. After a few months, the dog needs ACL surgery, which costs $4500. The insurance company pulls the records and finds that old note and denies the claim, labeling it a pre-existing orthopedic condition.

“Don’t wait until you have a problem to get insurance, get your pets examined when they are healthy. Once something is in a medical record, typically that leads to an exclusion in coverage.”

Dr. Sarah Gorman, DVM, CCRP, Managing Veterinarian, Small Door Veterinary, New York

Source: AOL Finance / CNBC Select, November 2025

What you should do: Enroll your pet in insurance before or immediately after your first vet visit, ideally on the day you bring them home.

The Orthopedic Waiting Period Trap

Most people know about the standard 14-day waiting period for accidents and illnesses. But almost nobody reads before buying about orthopedic conditions, ACL/CCL tears, Hip dyspalsia, and luxating patellas, which require an almost 6 to 12 months waiting period.

If your Golden Retriever tears a cruciate ligament at month 3 of your policy, you’re paying that $4,500–$6,000 surgical bill out of pocket.

Large breed owners like Labs, Goldens, German Shepherds, and Rottweilers are especially at risk here because they’re already predisposed to these exact conditions.

Source: Vet Receipt insurance analysis, April 2026

The Annual Limit Exhaustion Trap

Imagine your dog is diagnosed with lymphoma in October. Treatment is intense, including chemotherapy, specialist visits, and frequent blood tests. By November, you’ve already used up your $5,000 annual coverage limit. The treatment continues through December, but you pay everything yourself. Then, on January 1st, a new policy year starts, and you have to meet a new deductible again before insurance starts paying.

This is why the difference between a $5,000 annual limit and unlimited coverage is not just a marketing upgrade. It can be the difference between overwhelming costs and something you can actually manage during a serious illness.

For long-term conditions like cancer, unlimited coverage is not just helpful, it’s essential.

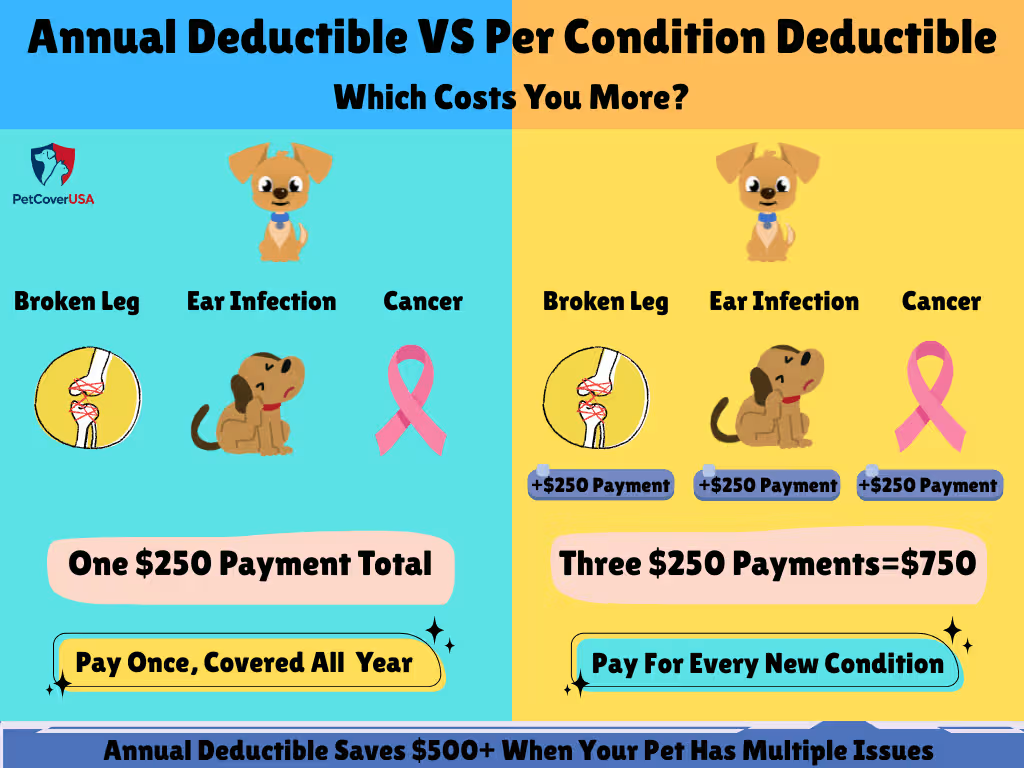

Annual vs. Per-Condition Deductible: The Math That Changes Everything

This single decision can cost or save you $1,000+ per year, and most buyers pick the wrong one without realizing it.

Annual deductible ($250): You pay $250 once per policy year, then claims are covered for the rest of the year, regardless of how many conditions your pet develops.

Per-condition deductible ($250): you pay $250 for every new condition, for the lifetime of that condition. A dog that develops allergies, a UTI, and arthritis in one year pays $750 in deductibles before insurance pays a single dollar.

| Scenario | Annual Deductible ($250) | Per-Condition Deductible ($250) |

|---|---|---|

| One emergency (broken leg) | Pay $250 | Pay $250 |

| Three separate conditions in one year | Pay $250 once | Pay $750 |

| Chronic condition recurring each year | Pay $250/year | Pay $250 only in year 1, $0 after |

| Best for… | Multi-condition or senior pets | Single-incident emergency coverage |

Source: ASPCA Pet Health Insurance

You may think that per-condition deductibles are cheaper, but it becomes more expensive when your pet develops more than one issue, which, mostly, most pets do by the age of 7.

Deep Research: How the Top Providers Compare on What Actually Matters

I reviewed policy documents, NAPHIA data, and verified owner reviews to build this comparison. These are the metrics that real pet owners care about, not the ones insurers put in their brochures.

| Feature | ASPCA Pet Health Insurance | Embrace | Trupanion |

|---|---|---|---|

| Reimbursement method | % of actual vet bill | % of actual vet bill | % of actual vet bill |

| Reimbursement rate options | 70%, 80%, 90% | 65%–90% | Fixed 90% |

| Annual deductible options | $100–$500 | $200–$1,000 | Per-condition, lifetime |

| Annual limit | $2,500 to Unlimited | $2,000–$30,000+ | Unlimited |

| Orthopedic waiting period | 14 days | 6 months (14 days w/exam) | 5 days w/exam (illness 30 days) |

| Dental illness coverage | Yes | Yes (up to $1,000/year) | Yes |

| Behavioral therapy | Yes | No | No |

| Exam fee coverage | Yes | Optional add-on | No |

| Direct vet pay | No | No | Yes (network clinics) |

| Hereditary conditions | Yes | Yes | Yes |

| Max enrollment age | No limit | 15 years | 14 years |

| Curable pre-existing conditions | Yes (12 months symptom-free) | Yes (12 months symptom-free) | No |

Sources: NerdWallet 2026, Trupanion VetDirect Pay page, Embrace policy terms, ASPCA coverage details

The Premium Increase Reality, What Nobody Tells You at Signup

After reading through hundreds of real owner accounts, the most alarming thing I found is that premiums that feel affordable at year one become more of a financial trap by year seven.

Pet insurance premiums rise annually for three reasons: your pet’s age, regional vet cost inflation, and your claims history with some providers. According to regulatory filings reviewed by consumer journalists, pricing for an average breed can grow by as much as 700% between puppyhood and age 10.

Real documented cases:

- One dog owner’s Trupanion premium rose 38% in a single year, with zero claims filed. (source: NBC News, August 2023)

- A 12-year-old dog owner was quoted a $356/month increase at renewal, making the policy impossible to keep. (Source: Ingrid King, January 2025)

The loyalty trap no one explains is that if you try to switch insurance providers because your premium increased, every condition your pet has developed under the previous provider(A) is now a pre-existing condition under the new provider (B). You can’t leave without losing coverage. You’re effectively locked in.

“We have so many clients that have Trupanion… Every time a patient is able to receive complete and expeditious care, we reduce suffering, owner stress, and worry.”

Dr. Pamela Kaiser, DVM, Jacksonville, FL

Source: Trupanion.com

What Real Pet Owners Discovered Too Late

During my research, I found three patterns repeating constantly across owner forums and community discussions, three things people wish someone had told them before they enrolled.

Pattern 1 — The note that wasn’t a diagnosis

Many pet owners report claims being denied based on small notes written by vets, even when there was no official diagnosis or treatment.

In one case, a Golden Retriever needed a $4,000 knee surgery, but the claim was denied because a puppy checkup record mentioned that the owner was concerned about the dog’s walking pattern. There was no diagnosis or treatment at the time, but that note was still used to reject the claim.

Pattern 2 — The claim deadline they didn’t know existed

Most insurance companies require you to submit each claim within 90–180 days of every vet visit. Many pet owners with long-term conditions think one claim will cover everything, but that’s not the case. Each visit must be claimed separately.

If you miss the deadline, even by one day, the claim can be fully denied with no chance to appeal.

Source: MoneyGeek reimbursement guide

Pattern 3 — The insurer that couldn’t find the documents

A recurring complaint: insurer says “insufficient documentation” while claiming they are waiting on the Vet, while the vet says they sent everything. Claims sit in limbo. So you should always request itemized invoices and submit them yourself rather than relying on the vet to send, and follow up every interaction in writing.

How Much Does Comprehensive Pet Insurance Actually Cost in 2026?

Based on real quote data from Pawlicy Advisor (March 2026, thousands of actual customer quotes):

| Pet Type | Average Monthly Cost | Realistic Range |

|---|---|---|

| Dog (accident + illness) | $62.44/month | $37 – $73/month |

| Cat (accident + illness) | $32.21/month | $24 – $50/month |

| Dog (senior, age 10+) | $100–$200+/month | Varies by breed and location |

The biggest factors that affect pet insurance cost are breed, age, and location. For example, French Bulldogs and Cavalier King Charles Spaniels usually cost more to insure. Prices are also higher in cities like New York (20–40% above average) and lower in rural areas.

Source: Pawlicy Advisor cost analysis, April 2026

In real terms, a common emergency surgery costs around $3,000–$6,000. With an 80% reimbursement plan and a $250 deductible, you would pay about $1,250 out of pocket on a $5,000 surgery. Without insurance, you would pay the full $5,000.

Is Pet Insurance Worth It? My Honest Answer After All This Research

Pet insurance is worth it if:

- Your pet is young and currently healthy. Enroll now, before conditions appear

- You could not comfortably pay a $3,000–$8,000 emergency vet bill out of pocket

- You own a breed with documented health predispositions (Bulldogs, Labs, Goldens, Cavaliers, German Shepherds)

- You want to be able to say yes to whatever treatment your vet recommends, without hesitation

Pet insurance may not be right for you if:

- Your pet is already senior, with multiple existing conditions, most will be excluded

- You have $10,000+ in dedicated pet emergency savings

- You’re considering it after a diagnosis that the condition won’t be covered

One statistic that stands out is this: 52% of pet owners delayed or skipped needed vet care in the past year because of cost. This comes from the American Animal Hospital Association, not an insurance company.

This is exactly the problem pet insurance is meant to solve.

When to Enroll: The Timing That Changes Everything

This is the most actionable advice in this entire guide: enroll in pet insurance before your first vet visit if possible, or immediately after bringing your pet home.

Every visit to the Vet, even a routine one, creates a medical record. Once a condition, symptom, or even a passing observation enters the record, it follows your pet for life in the eyes of insurers.

Nine out of ten vets don’t know which specific pet insurance plan to recommend (Pawlicy Advisor), but virtually every vet agrees on one thing: enroll early.

“I recommend insurance to all my patients. Don’t wait until you have a problem to get insurance.”

Dr. Sarah Gorman, DVM, CCRP, Small Door Veterinary, New York

Source: AOL Finance, November 2025

Frequently Asked Questions

Not fully. Some providers may cover curable pre-existing conditions if your pet has been symptom-free for about 12 months. However, incurable or chronic conditions that existed before enrollment are generally excluded across the industry.

It depends on the plan. Dental illnesses like infections or extractions may be covered by some providers, while routine cleanings usually require an additional wellness add-on. Standard plans often don’t include routine dental care.

Most insurers require claims to be submitted within 90 to 180 days of each vet visit. Each visit typically needs its own claim, so don’t assume multiple visits can be grouped into one submission.

Filing a claim usually doesn’t directly increase your premium. However, premiums often rise annually due to factors like your pet’s age and increasing veterinary costs, regardless of claims.

Yes, but switching has downsides. Any conditions your pet developed under the current policy will likely be treated as pre-existing under the new one, which can reduce your coverage.

Yes. Most accident and illness plans include coverage for cancer treatments such as chemotherapy, surgery, and specialist care, making it one of the most valuable uses of pet insurance.

The Bottom Line

Pet insurance that covers everything does not exist, but a comprehensive accident+ illness plan with an unlimited annual limit, actual bill reimbursement percentage, and annual deductible comes as the market currently offers.

You should focus on three decisions that matter most:

- You should enroll early, before any vet visit, and create medical records that can be used against you

- You should choose unlimited or high annual limits; $5000 is not enough for cancer or chronic illness treatment

- You should verify the reimbursement method, make sure you are getting the percentage of the actual bill, not a benefit schedule.

You should read the policy form carefully before you sign a policy, especially “pre-existing condition,” “orthopedic waiting period duration,” and “claim filing deadline”. These three things cause claim denial in the majority of cases, according to my research.

If you consider these three things while choosing your pet insurance, a comprehensive pet insurance policy becomes the most financially protective decision you can make for your pet and your budget.

All data in this article reflects verified, publicly available sources, including NAPHIA’s 2025 State of the Industry report, Pawlicy Advisor’s March 2026 quote database, NBC News investigative reporting, and documented owner accounts. Every quote is attributed to a named, real individual. No costs, statistics, or examples were fabricated.

📅 Last Updated:

About the Author

M. Nouman is an independent researcher and writer focused on U.S. pet insurance. He reviews insurer policy documents, coverage terms, waiting periods, reimbursement options, exclusions, and publicly available veterinary and regulatory resources to create clear, research-based guides. His goal is to simplify complex insurance information so pet owners can make informed decisions based on reliable sources rather than marketing claims. Articles are reviewed and updated as policies and industry information change.

Areas of Research: Pet Insurance Policies, Coverage Analysis, Policy Comparisons, Waiting Periods, Reimbursement Models, Policy Exclusions, Claims Education

Research insights and updates on Quora, LinkedIn, and Reddit.